- LOGIN

- MemberShip

- 2026-06-14 23:40:33

- Policy

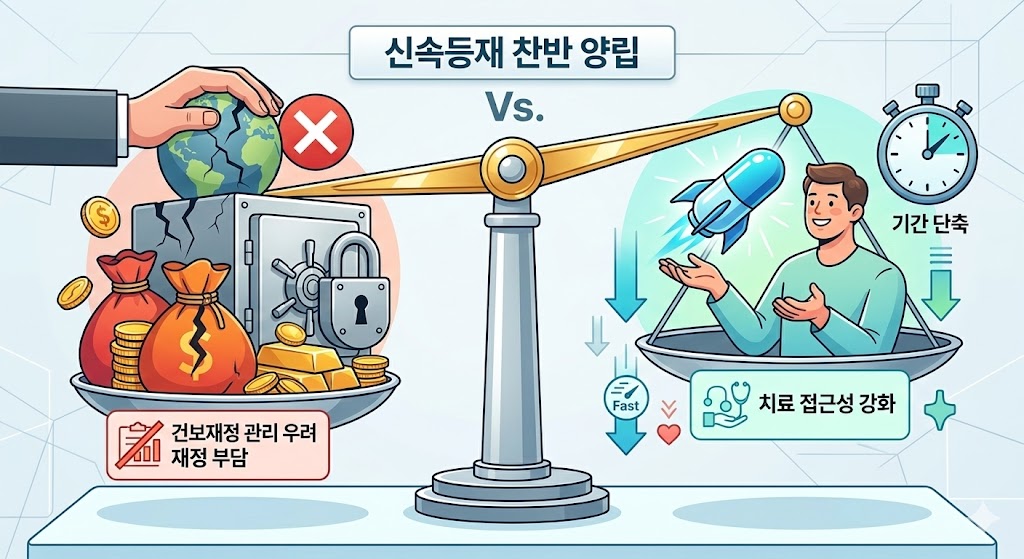

- Debate over fast-track listing of new drugs continues

- by Jung, Heung-Jun Mar 12, 2026 08:35am

- Debate continues over the proposed reform of the drug pricing system aimed at shortening the reimbursement listing period for new drugs. On one side are calls to strengthen treatment access, while on the other are concerns that the reform could sharply increase the burden on Korea’s national health insurance budget.While working bodies like HIRA are preparing to strengthen post-listing control, concerns persist about the effectiveness and potential side effects of expedited listing.The Korean Pharmacists for Democratic Society, which previously called for reconsideration of the fast-track listing initiative together with the Citizens' Coalition for Economic Justice (CCEJ) last month, plans to hold a briefing session next week to point out issues in the proposed new drug pricing reform.AI-generated imageOn the 10th, the Korea Alliance of Patient Organizations urged the government to promptly implement the fast-track listing and post-listing evaluation system, arguing that delays in national health insurance reimbursement after regulatory approval for anticancer drugs and rare disease treatments are reducing treatment accessibility.The government recently announced that starting in 2026, it will launch a pilot program for a “fast-track listing–post-evaluation system,” which would shorten the reimbursement listing period for rare disease treatments from the current maximum of 240 days to within 100 days. The alliance called for the swift implementation of the measures.KAPO emphasized, “Rather than blocking entry at the early stage, it is important to establish a sophisticated post-listing evaluation and management system based on treatment performance.”Until recently, attention surrounding the drug pricing reform had focused largely on price cuts for already-listed drugs, while the direction of the fast-track listing reform for new drugs received relatively less attention. The pharmaceutical industry, which has little reason to oppose faster market entry, had been cautiously waiting for details of the implementation plan.However, the issue gained prominence in February when groups including CCEJ, the Korean Association for Serious Diseases, and the Korean Pharmacists for Democratic Society urged reexamination of the fast-track listing policy. They also called for a public hearing on issues including raising the ICER threshold and introducing flexible drug pricing agreements.Criticism calling for broader social discussion is expected to continue this month. The Korean Pharmacists for Democratic Society is expected to hold a briefing on March 18 on the proposed new drug pricing reform and express opposition to the fast-track listing policy.An official from the organization said, “Although there are measures to evaluate outcomes and provide refunds if necessary, there are no clear post-management mechanisms, such as price reductions or market withdrawal, after post-evaluation. As the financial burden on the National Health Insurance is expected to surge, preparing countermeasures must be prioritized.”The official continued, “There are also doubts about whether strengthened post-listing management measures are appropriate for Korea. The briefing will address the impact of the overall new drug pricing reform, including fast-track listing.”Critics also argue that the reform of the new drug pricing system, like the proposed price cuts for generics, lacked sufficient prior discussion.A pharmaceutical industry official said, “As with the generic drug pricing reform, this situation arose because sufficient discussion was not conducted before the reform plan was announced. If there had been even a process to coordinate the implementation measures, the current backlash would not have occurred.”

- Company

- Quadrivalent meningococcal vaccine 'MenQuadfi' prescribed at gen hospitals

- by Eo, Yun-Ho Mar 12, 2026 08:35am

- Sanofi Korea's MenQuadfiThe quadrivalent meningococcal vaccine 'MenQuadfi' is now available by prescription at major general hospitals.According to industry sources, Sanofi Korea's MenQuadfi (Meningococcal Polysaccharide Tetanus Toxoid Conjugate Vaccine), indicated for the prevention of invasive meningococcal disease (serogroups A, C, Y, and W), has passed the Drug Committees (DC) of 23 medical institutions nationwide. These include tertiary general hospitals such as Seoul National University Hospital and Asan Medical Center, as well as medical institutions, including Kyung Hee University Hospital at Gangdong, Konkuk University Medical Center, National Medical Center, and Soonchunhyang University Hospital.MenQuadfi was approved in Korea last April, and this drug is given as a single-dose administration in individuals aged 6 weeks to 55 years.Notably, MenQuadfi is the only vaccine in Korea approved with proven efficacy against meningococcal serogroup A in infants aged 6 weeks to less than 24 months. A key feature of the product is its ready-to-use liquid formulation, which eliminates the need for reconstitution or mixing, thereby enhancing convenience for healthcare providers. The immunization schedule consists of four doses for infants aged 6 weeks to less than 6 months, two doses for those aged 6 months to less than 24 months, and a single dose for individuals aged 2 to 55 years.Meningococcal disease has been pointed out as a significant global public health concern. Classified as a Group 2 legal infectious disease with a fatality rate of approximately 10–14%, it affects 500,000 people worldwide annually.Primary symptoms include headache, fever, neck stiffness, vomiting, and altered consciousness, often accompanied by petechiae or purpura fulminans. The importance of prevention is signified by the fact that 11–19% of survivors suffer from long-term sequelae, including hearing loss, cognitive impairment, and neurological disorders.Since meningococcal disease is transmitted via respiratory droplets or direct contact, vaccination is highly recommended for individuals entering communal living environments. Typical candidates include military recruits and first-year college students who plan to live in dormitories.Furthermore, vaccination is advised for travelers or residents in high-incidence areas such as the African meningitis areas, as well as pilgrims traveling to Mecca, Saudi Arabia. Other recommended groups include individuals with immune system disorders, such as complement deficiencies, and those with anatomical or functional asplenia.Meanwhile, in clinical trials, MenQuadfi demonstrated non-inferiority across all four serogroups compared to existing quadrivalent meningococcal vaccines. Specifically, in the 10–55 age group, the seroprotection rates for MenQuadfi were 94.7% in Group A, 95.7% in Group C, 96.2% in Group W, and 98.8% in Group Y.Additionally, studies in children aged 2–9 years confirmed non-inferiority to existing quadrivalent vaccines, with seroprotection rates ranging from 86% to 99%. The vaccine also demonstrated stable immunogenicity when co-administered with other pediatric vaccines.

- Policy

- ‘Active INN prescribing needed for drugs with supply shortages’

- by Jung, Heung-Jun Mar 12, 2026 08:35am

- Han-sook Kim, Director of Health Insurance Policy Division, MOHWThe government said it is reviewing various measures while expressing support for introducing INN (international nonproprietary name) prescribing for drugs with unstable supply.It also stated that it will continue consultations to minimize the impact of the drug pricing reform plan on the field and will further refine the system even after implementation.On the 11th, Han-sook Kim, Director of the Health Insurance Policy Division at MOHW, stated at the National Assembly's drug pricing system discussion forum, " There are many concerns surrounding INN prescribing due to conflicting stakeholder interests. From the perspective of preventing supply instability, it is necessary to actively utilize INN prescribing. We are reviewing various aspects, including the criteria for supply instability and the safety, efficacy, and effectiveness of INN prescribing.”When asked about the direction of the drug pricing reform, Kim said the government would consider the policy’s impact on the field and remain open to consultations and improvements.Director Kim explained, ”The government is also paying close attention to the sustainability of the National Health Insurance finances. We are making multifaceted efforts. Improving unreasonable structures is crucial, and advancing the drug pricing system reforms is part of that effort.“Kim added, “This is an agenda with diverse perspectives. The government cannot clearly predict the impact the reform will have on the field once implemented. The government cannot clearly predict the impact on the field when drug pricing system reforms are implemented. Even after the reform is implemented, we will strengthen monitoring and make improvements if problems arise.”Kim dismissed concerns that the drug pricing reform plan concentrates insurance spending on multinational pharmaceutical companies, and said that it was a misunderstanding.Kim said, “The drug pricing reform could be misunderstood as a policy favorable to the global pharmaceutical industry. But promising companies and technologies must receive investment. If cost savings are generated through the reform, it will be used to properly reward companies investing in R&D.”

- Policy

- Doctors "If INN prescribing is enforced, will boycott the SPD"

- by Kang, Shin-Kook Mar 12, 2026 08:34am

- Doctors who took to the National Assembly to protest the promotion of International Nonproprietary Name (INN) prescribing legislation have said they will go as far as a total boycott of the Separation of Prescribing and Dispensing (SPD) system if the bill is enforced.On the 11th at 4:00 PM, the Korean Medical Association (KMA) Special Committee for public health promotion held a rally in front of the National Assembly Main Building in Yeouido to block the INN prescribing legislation.The doctors gathered at the National Assembly held pickets reading "Will Declare SPD System Annulment if INN Prescribing is Enforced" and demanded an immediate halt to the legislative process.At the scene, Kim Taek-woo, KMA president, emphasized, "INN prescribing is not merely about selecting a chemical component. It is a highly sophisticated professional medical act performed after considering the patient's comprehensive condition. This irrational bill, which prioritizes pharmacy inventory over patient needs when dispensing medication, must be scrapped immediately."The Korean Medical Association (KMA) Special Committee for public health promotion held a rally in front of the National Assembly Main Building in YeouidoKim warned the government and the National Assembly, saying, "Do not trade the public's health for economic logic. While pharmacist groups mislead public opinion by citing ambiguous budget savings, no budget can be more precious than the lives of our citizens."Kim further stressed, "If INN prescribing is enforced, we will regard it as a unilateral breach of the Medical-Pharmaceutical-Government Agreement and declare the total nullification of the SPD system. If our right to prescribe is violated and patient safety is threatened, we will stake everything, including my presidency, on this struggle."Following him, Kim Kyo-woong, Chairman of the KMA representative council, pointed out, "INN prescribing is not simply a systemic change. It is an act that denies the medical judgment of physicians who have precisely diagnosed a patient's condition. Furthermore, it is a highly irresponsible idea that breaks the continuity of treatment and puts patients at risk."Lee Ju-byung, Chairman of the Special Committee to Oppose INN Prescribing, asked, "The new bill states that failure to comply with mandatory INN prescribing will result in up to one year in prison or a fine of up to 10 million KRW. Is this such a serious crime? Who proposed that a doctor should face imprisonment for not prescribing by ingredient name?Lee raised his voice, saying, "Some say doctors prescribe by brand name to receive rebates," adding, "Then, are you advocating for INN prescribing just to receive rebates yourselves?"Lee added, "If the government insists on mandating INN prescribing for the sake of the public, we doctors will, in accordance with the government's will, launch a movement to prescribe only original drugs solely for the benefit of the people."Park Jong-hwan, President of the Medical Association Council for 25 clinics in Seoul, also noted, "On one hand, they say we must implement INN prescribing for public convenience, but on the other hand, they want to forcibly close large-scale pharmacies that the public can use late at night and which offer a wide range of drug choices," adding, "Isn't this an act of inconsistency?"Park stated, "The legislation proposed by Rep. Jang Jong-tae is a self-contradiction," adding, "Both bills contain the words public and patient, but the actual public and patients are nowhere to be found. They only look toward the interests and votes of specific professional interest groups."Park concluded, "I do not know whether it is a National Assembly member's job to pass bills that give all dispensing authority to pharmacists through INN prescribing and protect the interests of small pharmacy owners by regulating large pharmacies, or if this is simply for the benefit of a specific group."

- InterView

- ‘Broader access to CAR-T cell therapy needed for DLBCL’

- by Son, Hyung Min Mar 12, 2026 08:34am

- Diffuse large B-cell lymphoma (DLBCL) is a highly aggressive hematologic malignancy in which a significant number of patients achieve a cure with first-line therapy, but prognosis worsens sharply once relapse or treatment resistance occurs.In particular, patients who relapse or become refractory within 12 months after first-line therapy often struggle to achieve meaningful outcomes with conventional high-dose chemotherapy followed by autologous stem cell transplantation alone. Experts therefore stress the importance of shifting treatment strategies at an earlier stage.Against this backdrop, Gilead’s CAR-T therapy Yescarta (axicabtagene ciloleucel) is emerging as a new alternative based on clinical evidence accumulated in second- and third-line treatment settings.Professor Yun-seok Choi of Seoul St. Mary’s Hospital and Tony Li, Executive Director and Head of Medical Affairs at Kite International Region (Gilead’s oncology subsidiary), emphasized in a recent meeting with Dailypharm, “For DLBCL, the time to relapse and the number of treatment lines directly correlate with prognosis. This is why we must actively consider introducing CAR-T cell therapy at the second-line treatment stage.”Tony Li, Head of Medical Affairs at Kite International Region; Yun-seok Choi, Professor of Hematology-Oncology at Seoul St. Mary’s HospitalDLBCL is the most common subtype of aggressive non-Hodgkin lymphoma. Despite the standard first-line therapy R-CHOP (rituximab, cyclophosphamide, vincristine, prednisone), a substantial number of patients either relapse or become refractory to treatment.The problem is that after just one relapse, treatment response rates and survival prospects decline rapidly. High-dose chemotherapy and autologous hematopoietic stem cell transplantation, which have been the mainstay second-line therapy, require stringent patient selection and still carry a considerable risk of relapse even after treatment.In Korea, Yescarta was approved in August last year for DLBCL and primary mediastinal B-cell lymphoma (PMBCL), and its reimbursement criteria were established in January for third-line treatment by the Cancer Disease Deliberation Committee. However, reimbursement criteria for second-line use in patients who relapse or become refractory within 12 months of first-line therapy have not yet been established.Experts highlight unmet needs in the DLBCL treatment landscape, emphasizing the clinical value of Yescarta and the need for earlier CAR-T introduction in the second-line setting.Q. What are the practical difficulties or limitations of conventional treatments for DLBCL patients who relapse or become refractory after first-line therapy?[Professor Choi] Traditional second-line therapy consists of high-dose chemotherapy followed by autologous stem cell transplantation. However, this approach can only be applied to patients who meet certain conditions, such as being relatively young and having good overall health. Furthermore, relapsed DLBCL is often biologically aggressive, making treatment challenging.[Executive Director Tony Li] Standard first-line regimens like R-CHOP are highly effective, with about 70% of patients achieving a cure. However, treatment becomes increasingly difficult for patients with relapsed or refractory disease. Cure rates inevitably decline with each subsequent treatment line.Stem cell transplantation requires high-dose chemotherapy before the transplant, meaning patients must be in excellent physical condition to endure the entire process. They must be able to withstand the process of receiving anticancer treatment, responding to it, and then undergoing the transplant. Even among patients who successfully undergo transplantation, about 50% eventually relapse, and the prognosis for these patients is not optimistic.Q. In some countries, CAR-T or bispecific antibodies are reimbursed as second-line therapy. What clinical value does Yescarta have in real-world practice?Tony Li[Executive Director Tony Li] Yescarta has been approved in more than 20 countries and is recommended as a Category 1 option for second-line treatment of DLBCL in the National Comprehensive Cancer Network (NCCN) guidelines. This demonstrates that Yescarta has established itself as an evidence-based treatment option in the global clinical setting.Yescarta’s efficacy as a second-line therapy was demonstrated in the ZUMA-7 clinical trial. In this prospective controlled trial comparing Yescarta with standard stem cell transplantation therapy, Yescarta achieved results surpassing the existing standard therapy for the first time in 25 years. The median event-free survival (EFS), the primary endpoint, was 8.3 months in the Yescarta group, representing a significant improvement of approximately four times compared to the 2 months observed in the transplant group.It is also the first and only currently available CAR-T therapy to demonstrate statistically significant overall survival (OS) in a second-line setting.The drug also has accumulated meaningful long-term data. ZUMA-7 has accumulated nearly four years of follow-up data, showing a flattening of the OS curve. In the third-line setting, the 5-year follow-up results from ZUMA-1 confirmed that approximately 43% of patients survived, suggesting the potential for long-term survival.[Professor Choi] DLBCL is a disease with a high likelihood of death if the condition is not adequately controlled in the first line. This is the natural course of DLBCL observed in clinical practice.Even when high-dose chemotherapy followed by autologous stem cell transplantation is performed, the success rate is about 50%, meaning the number of patients rescued by this treatment is limited. In ZUMA-7, the OS curve for the standard-treatment group did not reach a complete plateau.In this context, Yescarta demonstrated statistically significant survival benefits compared to standard treatment, reducing the risk of death. Particularly significant is that CAR-T therapy has, for the first time in the history of DLBCL salvage therapy, presented survival data in a patient population with high mortality risk.Furthermore, the 5-year follow-up analysis of ZUMA-1 reported a 5-year OS estimate of 42.6% for patients treated with Yescarta. This suggests that approximately 4 out of 10 patients can expect long-term survival. Additionally, the fact that Yescarta demonstrated a survival benefit in the second-line setting in the ZUMA-7 study is also significant.Q. In January, reimbursement criteria for third-line Yescarta were established. How might this change third-line treatment strategies?[Professor Choi] Comparing the OS curves, Yescarta's data shows a relatively higher position compared to Kymriah (tisagenlecleucel). Although this was not confirmed through a direct head-to-head trial, many clinicians believe Yescarta may have stronger anti-lymphoma activity, not only in DLBCL but also in follicular lymphoma. This perception could influence drug selection decisions to some extent going forward.Another factor is that Yescarta transports cells to manufacturing facilities without freezing them, which reduces certain regulatory burdens associated with human cell handling permits (such as GMP) required for some CAR-T therapies, potentially enhancing accessibility from the healthcare provider's perspective. This characteristic could also influence future drug selection and market share to some extent.Q. I understand that some countries overseas have approved Yescarta’s reimbursement as a second-line treatment. What are the benefits of using Yescarta in second-line therapy?[Executive Director Tony Lee] In the A8 countries referenced by Korea for drug pricing, Yescarta is reimbursed for both second- and third-line treatments. Clinical study results have consistently shown that using CAR-T therapies at earlier stages is associated with superior treatment outcomes. This trend was reported in studies ranging from ZUMA-1 to ZUMA-7.Additionally, the ZUMA-12 study, which evaluated Yescarta's efficacy in the first-line treatment of LBCL patients, also yielded positive results. The ZUMA-23 study, comparing standard therapy with Yescarta in first-line treatment, is also underway.The healthier the T cells, the higher the likelihood of producing effective CAR-T therapies. This is because patients are less exposed to chemotherapy at earlier stages, meaning their overall condition is likely better, and their immune function is more preserved. These conditions provide the rationale for earlier use of CAR-T therapy, as better treatment outcomes can be expected when CAR-T is administered under such circumstances.Q. Why is reimbursement for Yescarta necessary in second-line treatment?Yun-seok Choi[Professor Choi] Yescarta is a therapy that has demonstrated clinical efficacy in the second-line setting through clinical studies. Based on this evidence, it is evaluated as a meaningful treatment option for clinicians.For immunotherapies that rely on T-cell activation, T-cell fitness is extremely important. While it is challenging to quantitatively assess a patient's T-cell status, this remains an area of ongoing research.Anticancer drugs used in lymphoma treatment are agents that can selectively affect lymphocytes. Therefore, the more a patient is repeatedly exposed to anticancer therapy, the more the fitness of the patient's T cells, which serve as the material for CAR-T, or the patient's own T cells that should attack cancer cells when dual-specific antibodies are administered, inevitably decreases.Considering this, T-cell–based immunotherapy should ideally be introduced earlier, when immune function is still relatively preserved. Applying CAR-T therapy under normal immune conditions can yield better treatment outcomes, offering advantages in terms of long-term patient prognosis and quality of life.Reimbursement decisions should also consider treatment outcomes rather than focusing solely on drug prices. Patients who responded well in the ZUMA-1 and ZUMA-7 studies were able to return to daily life and resume economic activity. Given the unique disease course and therapeutic innovation in DLBCL, reimbursement decisions should proceed more quickly.Q. With the emergence of various new drugs like bispecific antibodies and early-stage CAR-T cell therapy, treatment options have broadened. Specifically, what are the criteria for patient groups where early-stage CAR-T therapy is deemed more urgent and suitable than conventional standard therapy?[Professor Choi] Patients at the second-line treatment stage, particularly cases where patients relapse within 12 months after first-line therapy. Through large-scale clinical trials, only Yescarta demonstrated effective results in patients who relapse or become refractory within 12 months after first-line treatment. It is the sole option with an approved indication for this patient group. Bispecific antibodies currently lack prospective evidence focused specifically on this patient population.However, CAR-T is not an immediately available treatment, requiring turnaround time (TAT).Should evidence for bispecific antibodies accumulate in the future, making both options available, clinicians will need to carefully consider treatment strategies. A cautious approach is warranted, weighing CAR-T's TAT against the biological aggressiveness of DLBCL in the relapse patient population and the rationale for bispecific antibodies in this setting.Q: What insights do you believe the global experience accumulated with Yescarta could provide for the domestic treatment environment?[Executive Director Tony Lee] The approval of Yescarta as a third-line therapy in Korea is a significant advancement, which can serve as a starting point that can open new treatment opportunities for both patients and healthcare providers. As experience with Yescarta accumulates in the third-line setting, we expect Korean healthcare providers' understanding of the drug's efficacy and characteristics to deepen.In addition, real-world data (RWD) continue to accumulate globally, and this evidence may support future discussions on second-line reimbursement in Korea. Given that approval and reimbursement have already been granted in several countries, we anticipate that discussions in Korea will also proceed based on an evaluation of the drug's clinical value.Q. How do you expect the DLBCL treatment landscape to evolve?[Professor Choi] About 70% of DLBCL patients can expect cure, but the remaining 30% fall into a high-risk group. Future research will likely focus on more precise identification of high-risk patients and tailored treatment strategies based on risk level.In particular, we anticipate a shift where T-cell-based immunotherapies, such as CAR-T, move to earlier treatment lines and are introduced earlier for high-risk patients.

- Policy

- ‘Pricing reform should not be finalized without reporting to NA’

- by Lee, Jeong-Hwan Mar 11, 2026 08:29am

- Rep. Sunmin Kim of the Rebuilding Korea Party criticized the Ministry of Health and Welfare, saying it should not move forward with approving and implementing a drug pricing reform plan— which primarily involves lowering generic drug prices— by having it approved by the Health Insurance Policy Review Committee without reporting to the National Assembly.Kim effectively put the brakes on the ministry after it attempted to proceed with the March schedule for subcommittee and full meetings of the Health Insurance Policy Deliberation Committee (HIPDC) without including any mention of the drug pricing reform plan in its 2026 annual policy briefing to the National Assembly, despite the issue being of the utmost concern to the pharmaceutical industry.National Assembly Health and Welfare Committee Joomin Park of the Democratic Party of Korea also agreed with Kim on the need for a separate briefing on the reform plan. Addressing Health and Welfare Minister Eun Kyeong Jeong, Park said, “Because this is a very important issue, it would be appropriate to provide an additional briefing at the committee’s plenary meeting after concluding your discussions on the reform plan.”At the full committee meeting on the 10th, Minister Jeong responded affirmatively to Rep. Kim's procedural remarks and Chairman Park's request for an additional briefing on the drug pricing system reform plan, saying the ministry would comply.Consequently, it is highly likely that the MOHW will provide a separate briefing on the direction of the drug pricing system reform plan at the full committee meeting of the National Assembly's Welfare Committee this month (March), after subcommittee discussions and before the full committee vote.Currently, the ministry plans to hold a one-point HIPDC subcommittee meeting on March 11, followed by further discussion at another subcommittee meeting on March 18, before bringing the reform plan to the HIPDC plenary meeting on March 26 for approval. This plan includes lowering the pricing calculation rate for already listed generic drugs from the current 53.55% to the 40% range.The pharmaceutical industry has criticized the proposal as a mechanical, across-the-board “lawnmower-style” price cut, presenting 48% as their absolute bottom line for the generic drug calculation rate.With the gap between the MOHW and the pharmaceutical industry over the reform plan showing no signs of narrowing, Rep. Kim raised the issue through a procedural remark as the MOHW attempted to pass the plan without reporting it to the National Assembly.Rep. Kim stated, “After reviewing the MOHW's briefing materials, I question what the most pressing issue in current healthcare policy actually is. From what I understand, the drug pricing system reform is the topic most intensely discussed in the media and policy circles recently.”Kim continued, “I hear that tomorrow and next week, the HIPDC subcommittee will finalize the generic drug price reduction ratio. Following HIPDC deliberations at the end of March, discussions are proceeding with the goal of implementation next January. Yet, such an important policy report was not included among today’s key briefing items.”Kim added, “At this rate, there are concerns that the government could proceed with the drug pricing reform without reporting it to the relevant standing committee of the National Assembly. Therefore, I ask the Chairman to ensure that the MOHW clearly reports on the drug pricing system reform currently being pursued during today's briefing.”When Chair Park asked Minister Jeong whether she could provide an immediate briefing on the reform plan, Jeong replied, “We plan to hold about two more discussions in the HIPDC subcommittee to further coordinate opinions and gather more diverse input from the industry. As the proposal has not yet been finalized, we will review the progress and provide either a written report or a separate briefing.”In response, Park demanded that the MOHW prepare to provide an additional briefing at the committee’s plenary session, given the critical nature of the drug pricing system reform plan being pursued by the MOHW.Park stated, “Since additional processes and procedures remain (regarding the reform plan), individual briefings are fine, but because this is an extremely important issue, it would be better to provide an additional report at the committee’s plenary meeting once the discussions are complete.

- InterView

- [Reporter’s View] Precision over severity required for the GMP regulation

- by Hwang, byoung woo Mar 11, 2026 08:29am

- The system for revoking GMP (Good Manufacturing Practice) compliance certification is approaching a turning point.This policy, often referred to as a “one-strike-out” rule, reflects the government’s intention to apply a zero-tolerance principle against companies that obtain GMP certification through intentional data manipulation or fraudulent means.The system was born in response to incidents of arbitrary manufacturing, where companies falsified manufacturing records and produced drugs disregarding established procedures.The government’s intent is understandable. GMP is the most fundamental system underpinning trust in the pharmaceutical industry, and it is only natural that strict standards are applied to quality control in the manufacturing process.Some evaluations suggest that implementing this system has elevated the status of quality control organizations within pharmaceutical companies and provided an opportunity to reorganize their data and documentation management systems.However, as time passes, new questions have emerged in the field. There is growing reflection on whether strong regulations are actually functioning in a way that strengthens the quality culture.Some in the industry point out that the regulatory structure, which fails to sufficiently differentiate the types and severity levels of GMP violations, may not align with on-site realities.Questions are being raised about whether it is reasonable for intentional quality manipulation or serious manufacturing violations to be discussed within the same regulatory framework as simple management oversights, without distinguishing their relative gravity.For these reasons, discussions are currently underway in the National Assembly to amend the Pharmaceutical Affairs Act, proposing the introduction of intermediate measures within the system for revoking GMP certification. The core focus is on refining the units of administrative penalties that can be imposed for GMP violations beyond the current system.There is also growing interest in whether such discussions can preserve the intent of the system while adding greater regulatory precision.In fact, global pharmaceutical regulatory environments have recently been moving toward risk-based management. This approach determines the level of response by comprehensively considering factors such as the intent of the violation, its impact on patient safety, and the likelihood of recurrence.Compared to the US or Europe, which apply regulations in stages depending on the severity of the violation, the one-strike-out system has drawn criticism that it could excessively stifle the field, regardless of its necessity.Of course, this does not mean deregulation is the solution. Pharmaceutical quality regulation is an area where public trust can collapse from a single incident.Therefore, what matters more than the intensity of regulation itself is its precision. Quality regulation should function not as a system that stifles the field, but as one that strengthens a culture of quality.The GMP one-strike system also faces the same question. Beyond delivering a strong message, it needs to be examined whether it actually functions as a policy that improves real quality standards.Ultimately, what matters is not the mere existence of regulation, but the direction it creates. This reporter hopes that the proposed reform will bring the precision needed to both breathe life into the industry and safeguard the final bastion of pharmaceutical safety.

- Company

- SK Biopharmaceuticals' Chinese joint venture pushes for listing

- by Cha, Ji-Hyun Mar 11, 2026 08:28am

- SK Biopharmaceuticals’ Chinese joint venture appears to be accelerating preparations for an initial public offering (IPO). This follows SK Biopharmaceuticals’ board approval late last year for pre-IPO investment in the joint venture and changes to the clinical development contract for an improved drug candidate in China. Observers note that SK Biopharm can simultaneously expect the benefits of expanding its China business and increasing its stake value through the joint venture's listing.According to industry sources on the 10th, SK Biopharm's board of directors in November last year approved two agenda items: a crossover investment in its Chinese joint venture, Ignis, and amendments to the agreement for the clinical development in China of an improved new drug owned by Ignis. Both proposals passed with unanimous support from outside directors.Ignis serves as SK Biopharmaceuticals’ strategic outpost for the Chinese market. In 2021, SK Biopharmaceuticals established Ignis together with China-based global investment firm 6 Dimensions Capital (6D). At the time of its launch, Ignis raised USD 180 million in Series A funding, the largest Series A investment in China’s pharmaceutical industry that year. Investors included Ruentex Group, KB Investment, WTT Investment, Abu Dhabi sovereign wealth fund Mubadala Investment Company, HBM Healthcare Investments, and Goldman Sachs.At the time, SK Biopharmaceuticals transferred the China rights to 6 central nervous system (CNS) assets, including its self-developed epilepsy drug cenobamate and sleep disorder treatment solriamfetol, to Ignis and acquired equity worth USD 150 million in the venture. Under the contract, SK Biopharmaceuticals also secured revenue streams, including a USD 20 million non-refundable upfront payment, USD 15 million in milestone payments tied to development, approval, and sales stages, as well as sales royalties. As of the end of September last year, SK Biopharm held 41% of Ignis shares, making it the largest shareholder.Industry observers view the latest board approval as a signal linked to Ignis’s IPO plans. Crossover investments are typically a funding method used by unlisted companies preparing for IPOs to attract institutional investors. Considering Ignis is pursuing a listing, this crossover investment decision is interpreted as a move to enhance its corporate value and establish an investment foundation before the IPO. Ignis is known to have formed an advisory team and proceeded with IPO preparations around the first half of last year to pursue a listing on the Hong Kong Stock Exchange (HKEX).At the same time, the revision of the clinical development agreement for the improved drug is seen as a measure to accelerate clinical trials in China and secure a more efficient commercialization pathway. China’s regulatory system, particularly regarding clinical trial sponsors and approval procedures, is heavily localized, requiring development structures tailored to local requirements. Analysts say the flexible adjustment of the contract structure reflects an effort to expedite clinical development and regulatory approval in line with the local regulatory environment.Ignis Pipeline Overview (Source: Ignis)Market expectations place the potential Ignis IPO around the first half of this year. If Ignis successfully lists on the Hong Kong exchange as planned, its growth trajectory is expected to accelerate. The influx of IPO capital could strengthen short-term funding for the China launch of cenobamate and solriamfetol, while in the longer term supporting development of additional CNS assets transferred from SK Biopharm as well as Ignis’s own pipeline.Ignis secured favorable conditions for entering the Greater China market after receiving new drug application (NDA) approvals from China’s National Medical Products Administration (NMPA) in December last year for both cenobamate and solriamfetol. With over 11 million epilepsy patients in China, the market is estimated to be worth USD 1.1 billion as of 2024. The number of patients with obstructive sleep apnea is estimated to exceed 170 million. With the two approvals, Ignis aims to expand access to treatments for CNS disorders in Greater China and provide new therapeutic options for local patients.Ignis has also applied for authorized generics for cenobamate and solriamfetol as part of a strategy to secure early market share. Authorized generics are identical versions of the original drug marketed with the permission of the original drug’s company. T This strategy allows companies to respond to competing generics after patent expiration while simultaneously targeting the price-sensitive segments of the market.In addition to licensed assets, Ignis is advancing its own drug development programs. The company recently completed dosing of the first patient in a Phase I clinical trial of ‘IGS01’, its internally developed candidate for levodopa-induced dyskinesia (LID) in Parkinson’s disease. IGS01 is a small-molecule drug candidate belonging to the positive allosteric modulator (PAM) class targeting the M4 muscarinic receptor, which regulates brain neurotransmission. This development signifies Ignis's evolution beyond merely commercializing acquired assets into a CNS biotech company with its own pipeline and R&D capabilities.The benefits SK Biopharmaceuticals stands to gain from Ignis's growth are clear. As Ignis's largest shareholder, SK Biopharmaceuticals is expected to see the value of its stake rise to hundreds of billions of won. Furthermore, by securing the massive Chinese market, it can diversify its portfolio, moving beyond its current business structure that is heavily dependent on the United States, which accounts for more than 90% of its revenue.An SK Biopharmaceuticals official stated, “We understand that Ignis is preparing for a listing on the Hong Kong stock exchange, but the specific timeline is confidential and difficult to confirm.”

- Policy

- MOHW agrees to relax convenience store medicine policy

- by Lee, Jeong-Hwan Mar 11, 2026 08:28am

- The Ministry of Health and Welfare (MOHW) has cast a vote in favor of an amendment to the Pharmaceutical Affairs Act that legislates the '20-item limit' on the number of safe household medicine items, currently prescribed by the Pharmaceutical Affairs Act, to a Presidential Decree (Enforcement Decree) to allow for lower-level legislation.The Ministry also expressed support for a provision that eases the '24-hour operation' requirement, which is a mandatory registration criterion for sales outlets, in eup, myeon, and dong where there are no pharmacies or safe household medicine sales outlets.In addition, the Ministry presented a specific proposal to delay enforcement by one year from implementation date to prepare for various matters related to institutional improvement, such as the establishment of subordinate statutes.The bill currently under discussion is facing significant backlash from the pharmacist community, as it could lead to the complete removal of regulations on the number of safe household medicine items in convenience stores and to the expansion of the sale of general medicines outside pharmacies. However, with the competent MOHW expressing support, the likelihood of its passage has increased.In addition to the MOHW, the Korean Society of Oriental Pharmacy, the Korea Alliance of Patients Organizations, the Consumers Union of Korea, and the Korea Association of Convenience Store Industry also supported the legislation. The Korean Pharmaceutical Association was the only organization to oppose the bill.On the 10th, the amendment to the Pharmaceutical Affairs Act, proposed by Representative Han Ji-ah of the People Power Party, is planned to be tabled at the plenary session of the National Assembly's Health and Welfare Committee.Rep. Han Ji-ah's stands that fixing the number of safe household medicine items in the Pharmaceutical Affairs Act is hindering the ability to respond flexibly and administratively to changes in the pharmaceutical market and environment, as well as to public demand.This is the reason for introducing a bill that provides a delegation provision, allowing the number of safe household medicine items to be determined by Presidential Decree.Rep. Han's proposal also includes a provision to establish the basis for the installation and operation of a Pharmaceutical Policy Deliberation Committee under the Minister of Health and Welfare.Easing the 20-item upper limit on safe household medicine items... Ministry supports, Pharmaceutical Association opposesThe Ministry supported the provision delegating the regulation of the 20-item limit for convenience store medicines, which is currently fixed in the Pharmaceutical Affairs Act, to a Presidential Decree.The MOHW also submitted a supportive opinion on relaxing the 24-hour operation requirement and the registration criterion for sales outlets on a limited basis in eup, myeon, and dong areas where there are no pharmacies or safe household medicine sales outlets, to improve accessibility to safe household medicines.However, the MOHW stated that the enforcement date should be adjusted to 1 year after promulgation to prepare for various matters related to institutional improvement, such as the establishment of subordinate statutes.The Korean Society of Oriental Pharmacy also agreed with the amendment to reorganize the safe household medicine system.The Korea Alliance of Patients Organizations and the Consumers Union also supported it. The Consumers Union also expressed the view that it is appropriate to determine the regulation on the number of items through an Enforcement Rule, an Ordinance of the Ministry of Health and Welfare, rather than a Presidential Decree.The Korea Association of Convenience Store Industry supported the bill while suggesting a modification that would require the MOHW to designate the number of household medicine items after receiving advice from a committee.The Korean Pharmaceutical Association strongly opposed. They pointed out that although various systems to supplement medically underserved areas, such as public late-night pharmacies, health clinics, and the designation of special locations, are already in place, the management and operation of safe household medicine sales outlets and special locations remain insufficient.The Korean Pharmaceutical Association argues that, rather than indiscriminately expanding the convenience store medicine system, the priority should be to evaluate whether the management systems of existing programs are functioning properly and to reorganize the system to ensure safe use.The Korean Pharmaceutical Association stated, "To resolve the pharmacy accessibility of residents in medically underserved areas such as farming and fishing villages, special locations can already be designated according to the Pharmaceutical Affairs Act, and a system is in place to allow the purchase of medicines through designated special locations. Currently, medicine is also accessible through 1,895 health clinics nationwide," and emphasized, "In particular, considering the increase in cases of acetaminophen poisoning, the lack of management of sales outlets and the increase in cases of non-compliance with requirements, and the trend of strengthening regulations abroad, we actively oppose the expansion of safe household medicine items at this point as it is a policy that directly contradicts national health."Establishment of Pharmaceutical Policy Deliberation Committee...Ministry of Health and Welfare, Ministry of the Interior and Safety, etc., all opposedThe MOHW and the Ministry of the Interior and Safety opposed the provision establishing a Pharmaceutical Policy Deliberation Committee, arguing that it would create an environment in which pharmaceutical-related matters, such as medicines, could be discussed regularly.The logic is that, since the Central Pharmaceutical Affairs Council exists and is established, installed, and operated by the MFDS, the establishment of an additional body is unnecessary.The Ministry of the Interior and Safety stated, "The Pharmaceutical Policy Deliberation Committee is an advisory committee under the MOHW, but considering the purpose of the Act on the Establishment and Operation of Committees Under Administrative Agencies, it is necessary to consider plans to expand the functions of the Central Pharmaceutical Affairs Council or utilize the policy advisory committees within the MOHW rather than establishing a separate committee."The Korean Pharmaceutical Association and the Korean Medical Association also submitted opposing views.The Korean Pharmaceutical Association opposed it, stating, "The role of the Pharmaceutical Policy Deliberation Committee in the bill is managed by the Pharmaceutical Policy Division of the MOHW," adding, "The policy planning and drafting are performed by the Ministry's Division of Pharmaceutical Policy, while the Pharmaceutical Policy Deliberation Committee performs policy deliberation and advice. In practice, this would lead to discussing the same matter twice, causing inefficiency and making the responsibility and subject of policy decisions unclear."The Korea Medical Association said, "Since the Central Pharmaceutical Affairs Council (CPAC) is already running, establishing a separate Pharmaceutical Policy Deliberation Committee would be a redundant installation of a committee performing similar functions, which is a waste of administrative power," adding, "There are concerns that it could lead to role conflicts between committees and inefficiency in the policy-making process."

- Company

- 'Datroway' launches in Korea…breast cancer ADC

- by Son, Hyung Min Mar 11, 2026 08:28am

- A Trop-2-directed antibody-drug conjugate (ADC), Datroway, obtained domestic approval, introducing a new treatment option to breast cancer. Based on clinical results, which show improved progression-free survival (PFS) compared with existing cytotoxic anticancer drugs. Attention is drawn to the possibility of expansion of the TROP2 ADC-based treatment strategy to triple-negative breast cancer (TNBC) beyond HR+/HER2- breast cancer.ADC anticancer drug 'Datroway'According to industry sources on the 11th, the Ministry of Food and Drug Safety (MFDS) approved Datroway (datopotamab deruxtecan), developed by AstraZeneca and Daiichi Sankyo, as a breast cancer treatment.The specific indication is hormone receptor (HR)-positive, human epidermal growth factor receptor 2 (HER2)-negative breast cancer.AstraZeneca paid $1 billion (approx. KRW 1 trillion) in upfront fees alone to secure the development rights for Datroway from Daiichi Sankyo in 2020. The total contract value, including development and commercialization milestones, amounts to $6 billion (approx. KRW 7 trillion).Datroway's target TROP2 is rapidly emerging as a core target in global ADC development.The TROP2 protein is known to be overexpressed in various cancer types, including breast cancer and non-small cell lung cancer (NSCLC). Datroway's mechanism of action involves binding to this protein and delivering cytotoxic drugs directly inside cancer cells to induce apoptosis. It is designed to maintain the efficacy of conventional cytotoxic chemotherapy while reducing damage to healthy cells.The basis for this approval is the Phase 3 TROPION-Breast01 study. This study was conducted on 732 patients with unresectable or metastatic HR-positive, HER2-negative breast cancer.Patients were randomized 1:1 into the Datroway group (365 patients) and the physician's choice of chemotherapy (TPC) group (367 patients).Datroway was administered intravenously at a dose of 6 mg/kg every three weeks, while the control group received an investigator's choice of chemotherapy among eribulin, capecitabine, vinorelbine, or gemcitabine.Primary endpoints included progression-free survival (PFS) and overall survival (OS) as assessed by Blinded Independent Central Review (BICR) according to RECIST 1.1 criteria. Objective response rate (ORR), duration of response (DOR), and disease control rate (DCR) were set as key secondary endpoints.The median PFS in the Datroway group was 6.9 months. This was an improvement over the 4.9 months in the chemotherapy group, reducing the risk of disease progression or death by 37%.The ORR was 36.4% in the Datroway group and 22.9% in the chemotherapy group, while the median DOR was 6.7 months and 5.7 months, respectively.Median OS was 18.6 months in the Datroway group and 18.3 months in the chemotherapy group, with no statistically significant difference at the time of analysis.In terms of safety, the most commonly reported adverse events were stomatitis, nausea, fatigue, alopecia, constipation, vomiting, and dry eye.Serious adverse events occurred in 3.1% of patients treated with Datroway. Major serious AEs included interstitial lung disease (ILD, 1.1%), vomiting (0.6%), diarrhea (0.6%), and anemia (0.6%). Fatal outcomes occurred in 0.3% of patients, with ILD cited as the cause.Potential as a first-Line treatment for triple-negative breast cancer (TNBC)TROP2-targeted ADCs are creating a new competitive landscape in breast cancer treatment. Currently, the first drug of this mechanism to be commercialized is Gilead's 'Trodelvy' (sacituzumab govitecan). Trodelvy has been approved for the treatment of TNBC in the U.S., Europe, and South Korea.Datroway has entered the market, pursuing indication expansions focused on breast cancer and non-small cell lung cancer.Both treatments show promise as first-line treatments for TNBC.In previously untreated metastatic TNBC, primary treatment options have been limited, except for the immune checkpoint inhibitor 'Keytruda' (pembrolizumab). Analysis suggests that, for PD-L1-negative patients who lack other options besides chemotherapy, the role of TROP2-targeted ADCs is likely to expand.In the Phase 3 TROPION-Breast02 study, Datroway significantly improved both PFS and OS compared with conventional chemotherapy in the first-line treatment of metastatic TNBC, where immunotherapy is difficult.The study results showed a PFS of 10.8 months for the Datroway group and 5.6 months for the chemotherapy group, nearly a twofold difference. OS was 23.7 months and 18.7 months, respectively, and both metrics were statistically significant.ADC anticancer drug 'Trodelvy'Trodelvy also demonstrated efficacy. The Phase 3 study, named ASCENT-03, compared Trodelvy with chemotherapy.In the study, Trodelvy had a median PFS of 9.7 months, compared with 6.9 months for chemotherapy. It was also shown to reduce the risk of disease progression or death by 38%.While OS was not yet mature at the time of the primary analysis, a trend of a continuously widening gap in PFS2 between the treatment and control groups has been confirmed, raising the possibility of future OS improvement.Gilead is also conducting the ASCENT-04 study to evaluate the efficacy of the Trodelvy + Keytruda combination. This combination has reportedly achieved PFS improvement compared to chemotherapy + Keytruda. Expects suggests that Trodelvy + Keytruda is highly likely to become the new standard of care for first-line TNBC treatment, regardless of PD-L1 expression levels.