- LOGIN

- MemberShip

- 2026-06-14 23:40:33

- Opinion

- [Desk’s View] On exempting innovative pharmas from price cuts

- by Lee, Tak-Sun Mar 10, 2026 08:56am

- Fostering the pharmaceutical and biotech industry while ensuring the soundness of the national health insurance budget is no easy task.The two are intertwined like a double-edged sword. Cutting drug prices indiscriminately to save money risks stifling the industry, yet allowing skyrocketing drug prices to go unchecked in the name of industry growth will quickly drain the health insurance coffers.That is why the government’s push to cut generic drug prices is undoubtedly a card played as the health insurance coffers are running dry. Yet, it is equally impossible to neglect the pharmaceutical and biotech industry, which is only now beginning to gain stature.The ‘Korea Innovative Pharmaceutical Company’ certification system emerged after long deliberation between fostering industry and maintaining fiscal soundness. The government aimed to identify and nurture the so-called ‘pharmaceutical companies capable of developing new drugs’ through this certification.However, 15 years have passed since the system's establishment in 2011, and one can't help but wonder if it has effectively achieved its original goal of fostering companies. The number of certified innovative pharmaceutical companies has now risen to 49, yet very few have developed drugs capable of competing on the global stage.The pharmaceutical industry claims the current certification doesn't offer ‘significant enough benefits to push promising companies forward.’ Rather, it's seen as merely ‘enough to keep them afloat within their group.’The most significant benefit pharmaceutical companies perceive from the Innovative Pharmaceutical Company certification is preferential drug pricing. Holding this title grants preferential treatment in pricing calculations for first generics or incrementally modified new drugs. For instance, while a standard company's first generic listing is priced at 59.5% of the highest price, an Innovative Pharmaceutical Company can set its price at 68%. Considering that drug prices directly translate to sales revenue, this means that certified companies can earn 7.5% more than non-innovative companies.However, this pricing preference is only a temporary benefit. After one year, the premium disappears, and “non-innovative” pharmaceutical companies end up with the same drug prices as the certified innovative ones.Even so, starting from the same line with even a slightly higher price is undeniably advantageous. This is why many pharmaceutical companies celebrate or despair over the results of the innovative pharmaceutical company review, which takes place every two years.If the innovative pharmaceutical company certification system is to better fulfill its purpose of ‘screening and fostering’ firms, the direction should be to tighten the review standards while expanding the benefits.In other words, the government should identify companies that truly have the capability to develop new global drugs while providing full support until they actually develop them.Some argue that innovative pharmaceutical companies should be exempt from unilateral price cuts made for listed drugs. From the perspective of fostering domestic pharmaceutical companies, this isn't entirely wrong. But would any company spend tens or hundreds of billions of won on new drug R&D while facing the risk of declining sales just to be saved from price cuts on existing drugs? Just for the title of being a certified innovative pharmaceutical company?However, even such benefits, if granted only to the 49 certified innovative pharmaceutical companies, would trigger backlash from non-innovative companies. There is already distrust in the field regarding the standards used to certify innovative pharmaceutical companies.But still, current discussions on drug price cuts for already-listed products and on reforming the innovative pharmaceutical company system need to be somewhat aligned. Rather than pushing through generic drug price cuts in a hasty manner despite strong opposition from the industry, perhaps it would be better to take a little more time and discuss them along with substantive benefits for innovative pharmaceutical companies. At the same time, the criteria for selecting innovative pharmaceutical companies should be reorganized so that they are truly centered on companies that genuinely engage in R&D.From a cautious standpoint, that may be the only way to both foster the industry and maintain health insurance sustainability.

- Policy

- Contaminated COVID vaccines, national petition for special investigation

- by Lee, Jeong-Hwan Mar 10, 2026 08:55am

- Minister of Health and Welfare Jeong Eun KyeongFollowing confirmation by disease control authorities of negligence in the management of foreign substances in COVID-19 vaccines, a national petition has been filed requesting the appointment of a Special Prosecutor to investigate the allegations.With multiple opposition lawmakers raising accountability issues against Minister of Health and Welfare Jeong Eun Kyeong, attention has been drawn to the progress of the petition.On the 6th, a petition was field on the National Assembly's e-People service stating, "We request the introduction of a Special Prosecuter to clearly investigate the foreign substance issues reported during the COVID-19 vaccine management process and the appropriateness of the administrative response."The petitioner demanded a Special Prosecutor investigation into the entire process of reporting and responding to foreign substances in COVID-19 vaccines. The request includes verifying the legality of reporting, recall, and quality control procedures; determining accountability; and conducting a full-scale investigation into potential external pressure or conflict-of-interest involvement.Furthermore, the petitioner urged the National Assembly to disclose the full results of the investigation, improve systems to prevent recurrence, and restore the public's right to know and trust in public health.According to the 'Diagnostics and Analysis of COVID-19 Response Status' report released by the Board of Audit and Inspection of Korea (BAI) on the 23rd of last month, the Korea Disease Control and Prevention Agency (KDCA) failed to notify the Ministry of Food and Drug Safety (MFDS) of foreign substance reports. Instead, they handled the issue by informing only the manufacturers and did not suspend vaccination with the same batch numbers despite the risk.Specifically, between March 2021 and October 2024, the KDCA received 1,285 reports of foreign substances in COVID-19 vaccines from medical institutions but bypassed the MFDS, opting to receive investigation results directly from manufacturers.While the majority of these cases (835, 65%) involved rubber stopper fragments due to usage errors, 127 cases (9.9%) involved hazardous foreign substances, including mold, hair, and silicon dioxide.Notably, because no suspension of administration was ordered for the vaccines containing hazardous substances, approximately 14.2 million doses from those specific batch numbers continued to be administered even after the reports were made.Based on the BAI announcement, the petitioner argued, "There is a need for an independent verification of potential deficiencies in the management and reporting systems, and whether the actions of the KDCA and MFDS complied with relevant laws and manuals," adding, "An objective investigation is also required regarding whether external pressure or conflict-on-interest interests influenced policy decisions during the reporting and management process."The petitioner further asserted, "It must be clarified whether the administrative agency's judgments were made based on public health principles or influenced by specific organizations or companies. Given that this matter directly affects national health, it is difficult to restore trust solely through internal executive branch investigations. The facts and accountability must be clarified through an investigation independent of political interests."Separate from the national petition, the opposition party is holding the Minister of Health and Welfare accountable for the contaminated COVID-19 vaccines.The People Power Party (PPP), citing the BAI report that contaminated vaccines were administered due to management failure during the pandemic, requested that Rep. Choo Mi-ae (Democratic Party), Chairperson of the Legislation and Judiciary Committee, cooperate in holding an emergency inquiry.Shin Dong-wook, Senior Supreme Council Member of the PPP, pointed out during a Supreme Council meeting on the 5th, "We requested the Democratic Party to hold an emergency inquiry into the BAI at the Legislation and Judiciary Committee, but Chairperson Choo is refusing, stating without reason that the committee cannot be convened."Rep. Na Kyung-won, the designated opposition lead for the Legislation and Judiciary Committee, also posted on Facebook yesterday, "According to KDCA data, there were 485,576 reports of adverse reactions, 2,802 deaths, and 1,285 reports of foreign substances. However, vaccinations were not stopped." Rep. Na added, "I will demand an emergency meeting of the Legislation and Judiciary Committee, the immediate withdrawal of government appeals [in vaccine lawsuits], the resignation of former Commissioner Jeong, and a parliamentary investigation."Rep. Kim Mi-ae, the PPP executive secretary of the Health and Welfare Committee, also stated at a PP meeting, "The status of COVID-19 vaccine management is a total failure that seriously threatens national health. It is a clinical experiment conducted by the state on innocent citizens." Rep. Kim urged Minister Jeong, who was the KDCA Commissioner at the time, to "take immediate responsibility, resign, and fully cooperate with the investigation."

- Policy

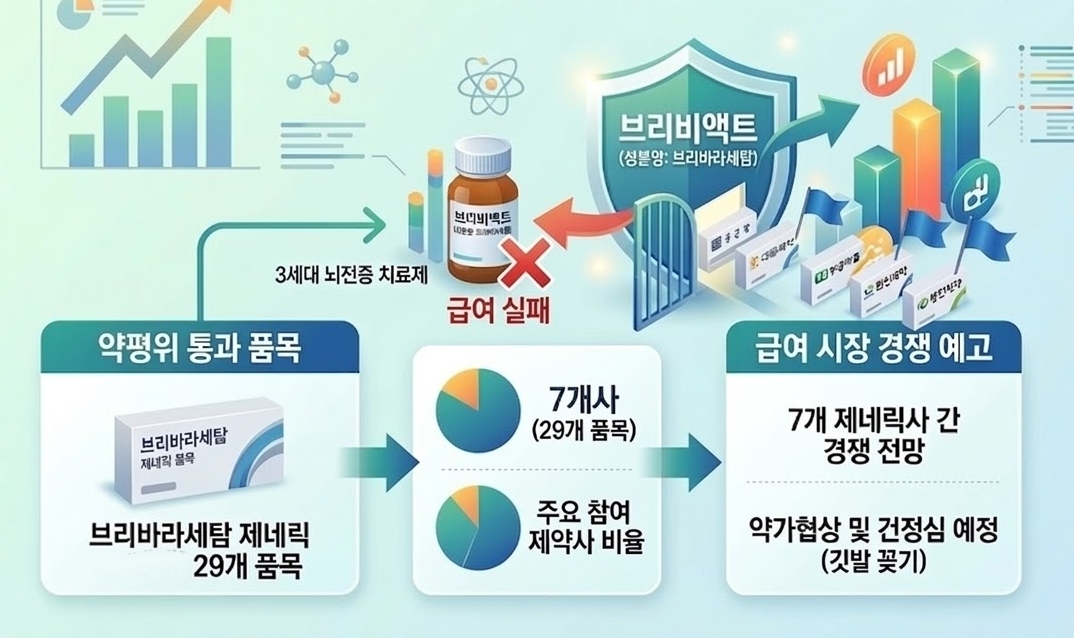

- Will Briviact become the next Vimpat? Generics near early listing

- by Jung, Heung-Jun Mar 10, 2026 08:55am

- Attention is focusing on whether generics will be listed first in the reimbursement market, in which the third-generation epilepsy treatment Briviact (brivaracetam) failed to enter.If 7 generic manufacturers, including Chong Kun Dang, Daewoong Pharmaceutical, and Samjin Pharmaceutical, secure reimbursement listing, competition among generic companies is expected in the reimbursed market without the original drug.Generic companies targeting Briviact’s vacancy are on the verge of securing reimbursement listing. AI-generated image.On the 5th, the Drug Reimbursement Evaluation Committee recognized the reimbursement adequacy of 29 epilepsy treatment products containing brivaracetam from 7 domestic pharmaceutical companies. Chong Kun Dang (Briveta Tab), Daewoong Pharmaceutical (Brivatop Tab), Bukwang Pharmaceutical (Bukwang Brifil Tab), Whanin Pharm (Briva Tab), Samjin Pharmaceutical (Bricetam Tab), Myung In Pharmaceutical (Buripam Tab), and Hyundai Pharmaceutical (Brilact Tab) are expected to proceed with listing procedures after price negotiations and review by the Health Insurance Policy Deliberation Committee. The original product is UCB Korea's Brivact, which received domestic approval in 2019. However, it failed to secure reimbursement listing when attempting to enter the insurance market and reportedly did not submit post-marketing surveillance (PMS) data last year. With its patent expiring last February, a series of generic approvals followed. Having passed the DREC hurdle, the generic versions are now on the verge of entering the reimbursement system.If price negotiations are finalized, a unique scenario could unfold where generics secure reimbursement listing before the original drug.Should generics gain early listing, it would mirror the case of UCB Pharma's other epilepsy treatment, ‘Vimpat (lacosamide)’.Vimpat, which was approved in Korea in 2010, ultimately failed to obtain reimbursement listing due to pricing issues, while generic versions of companies such as SK Chemicals’ Vimsk entered the reimbursement market first.According to the market research institution UBIST, Vimsk recorded sales of KRW 4.5 billion last year, marking 32% growth from KRW 3.4 billion the previous year. Its prescription performance has steadily increased over 4 years, from KRW 2.3 billion in 2021.The 7 companies preparing to list brivaracetam generics are also expected to attempt market entry using the same formula.The ultimate question is whether they can clear the drug price hurdle that the original failed to overcome.

- Opinion

- [Reporter’s View] Era of drugs better known than diseases

- by Son, Hyung Min Mar 10, 2026 08:55am

- A notable shift has recently emerged in clinical practice where drug names are increasingly being known before the diseases they treat.For example, when discussing obesity treatment, many people now think first of ‘Wegovy (semaglutide)’ or ‘Mounjaro (tirzepatide)’ rather than the disease itself. A similar trend is emerging for major immune disorders like atopic dermatitis. This change is also evident in the field of cancer treatment. It is now commonplace to hear specific drug names mentioned before the broader category of immuno-oncology drugs.Whereas diseases were traditionally recognized first, followed by treatments, we now frequently see drugs becoming symbolic markers that define or represent the disease itself.This shift cannot be explained simply by increased brand recognition. As more new drugs actually shift treatment paradigms, these therapies have taken on the role of driving disease awareness.For certain conditions, the emergence of specific treatments has altered diagnostic and therapeutic strategies, leading the drug name to become synonymous with the disease's treatment.The role of pharmaceutical companies has also evolved. Whereas disease awareness preceded the introduction of treatments, it is now common for disease awareness activities to proceed alongside new drug development. With treatment development and disease education occurring simultaneously, the drug name naturally becomes central to shaping disease awareness.The shift does have positive aspects. When innovative treatments emerge for diseases with limited therapeutic options, they inherently attract patient and clinician attention, serving as catalysts for heightened disease awareness. Indeed, for some conditions, social awareness of diagnosis and treatment has increased significantly following the introduction of such drugs.However, there are also concerns. If the structure where drug names become known before the disease itself solidifies, there is a risk that awareness could center around specific treatments rather than fostering a deeper understanding of the disease itself. While medicine inherently evolves through diverse treatment strategies and multiple options, public perception can be simplified around a single brand name.The influence of new drugs continues to grow. At the same time, the role of the pharmaceutical industry is expanding beyond developing therapies to shaping disease awareness itself. This means companies are becoming entities that shape disease perception, going beyond just treatment developers.Consequently, the social responsibility that the pharmaceutical industry must shoulder is also growing. As the influence of new drugs expands, so does the need to examine how this power operates and what its implications mean for the healthcare environment and patients. Now that pharmaceutical innovation can reshape disease awareness itself, the industry must consider its public responsibility towards patients and society, alongside its private corporate interests.

- Policy

- Entering into RSA contracts is the key to high-cost drugs

- by Jung, Heung-Jun Mar 10, 2026 08:55am

- As the number of ultra-high-cost new drugs seeking insurance coverage grows, more medications are entering double or triple Risk-Sharing Agreement (RSA) contracts.There is a growing trend of triple RSA contracts that combine the standard RSA Refund model with Expenditure Caps and Patient-Level Outcome-Based Refunds.AI-generated imageAccording to industry sources on the 5th, ultra-high-cost drugs recently listed are entering the reimbursement bracket through contracts that combine existing Refund and Expenditure Cap models with Outcome-Based Refunds.The government is strengthening these safety measures to manage financial risks while ensuring access to new drugs; in effect, these hybrid models have become an essential option for crossing the reimbursement threshold.A majority of the new drugs listed or granted expanded coverage this month involved hybrid contracts. Antengene's Xpovio (selinexor) and AstraZeneca Korea's Imjudo and Imfinzi were all subject to both Refund and Expenditure Cap models.For Xpovio, the additional financial requirement due to expanded coverage was estimated at KRW 11.6 billion. However, the government determined that the actual financial impact would be lower when applying two types of RSA.GC Biopharma's Livmarli (maralixibat), a treatment for pruritus in Alagille syndrome, was subject to a triple contract: a Refund, an Expenditure Cap, and a Patient-Level Outcome-Based Refund.The Patient-Level Outcome-Based Refund model tracks treatment results; if pre-agreed targets are not met, the pharmaceutical company must refund a certain amount. It is reported that Livmarli passed the Drug Benefit Evaluation Committee and the Health Insurance Policy Deliberation Committee because GC Biopharma submitted a risk-sharing plan that included this outcome-based refund.Ipsen Korea's Bylvay (odevixibat), a treatment for pruritus in patients with cholestatic liver disease listed last October, is another case of a triple contract.During its cost-effectiveness evaluation, Bylvay was found to have higher annual costs than alternative treatments. However, it was able to clear the listing threshold through the risk-sharing types proposed by the pharmaceutical company. At the time, the estimated annual claim amount was KRW 118.4 billion, but the financial burden was deemed lower through the RSA.As the listing and expansion of reimbursement for immuno-oncology drugs and high-cost new drugs continue to increase, pharmaceutical companies are actively using combinations of Refund, Expenditure Cap, and Outcome-Based Refund models to obtain National Health Insurance coverage.

- Policy

- Adstiladrin receives expedited review in Korea

- by Lee, Tak-Sun Mar 09, 2026 08:53am

- The gene therapy for bladder cancer ‘Adstiladrin,’ developed by Swiss company Ferring Pharmaceuticals, has been selected for Korea’s GIFT program, enabling expedited regulatory review by the Ministry of Food and Drug Safety (MFDS).The drug is the world’s first gene therapy for bladder cancer and received U.S. FDA approval in 2022.The MFDS announced on the 6th that Adstiladrin (nadofaragene firadenovec) has been designated as a drug eligible for fast-track review. The designation date was February 4th.The therapy has been submitted for approval in Korea for the treatment of high-risk non–muscle-invasive bladder cancer (NMIBC) that is Bacillus Calmette-Guerin (BCG)-unresponsive with carcinoma in situ (CIS), with or without papillary tumors.The MFDS designated the drug for fast-track review, citing improved efficacy compared with existing treatments. It had previously also been designated as an orphan drug.Adstiladrin also underwent fast-track review during the U.S. FDA approval process, leading to its accelerated approval. The therapy exerts its antitumor effect through the expression of the interferon alpha-2b (IFNα2b) gene delivered via a non-replicating adenovirus vector, administered intravesically.The GIFT program is a Global Innovative products Fast-Track Review Program designed to support the development of innovative medical products in Korea and has been in operation since September 2022.Eligible products include innovative medicines targeting life-threatening diseases, rare diseases with no existing treatment alternatives, and new drugs developed by certified Korea Innovative Pharmaceutical Companies.The MFDS conducts a comprehensive evaluation of the candidates’ innovative therapeutic benefits, contributions to addressing public health crises, and the developer’s efforts, among other factors.Adstiladrin has been designated as GIFT No. 65. Among the 50 products approved under the GIFT program so far, 42 are orphan drugs.

- Policy

- Health and Welfare Committee to conduct inquiries on pending issues next week

- by Lee, Jeong-Hwan Mar 09, 2026 08:53am

- The ruling and opposition party leaders of the National Assembly's Health and Welfare Committee have agreed to hold a plenary session on the 10th of next week to receive this year's (2026) business reports and conduct inquiries on pending issues.The committee plans to hold the First and Second Subcommittees for Legislations on the 11th and 12th, respectively, to process pending legislation. Following this, the bills are expected to be approved during a plenary session on the 13th and forwarded to the Legislation and Judiciary Committee.Key issues to be highlighted during next week's plenary session include the findings regarding contaminated COVID-19 vaccines and the proposed restructuring of the drug pricing system, which includes price cuts for generics and preferential pricing for innovative pharmaceuticals.Other pressing topics include policies to strengthen regional, essential, and public healthcare, such as increasing medical school quotas, establishing new regional·public medical schools, and implementing a regional physician system.The opposition, led by the People Power Party, is expected to take issue with Minister of Health and Welfare Jung Eun Kyeong's failure to publicly announce cases of COVID-19 vaccines containing mold or foreign substances during her previous leadership as Commissioner of the Korea Disease Control and Prevention Agency (KDCA). They are likely to demand a parliamentary investigation.Rep. Kim Mi-ae, the executive secretary of the committee, along with Rep. Na Kyung-won and Rep. Shin Dong-wook, are strongly calling for Minister Jung’s immediate resignation. They are also demanding that the government drop its appeals against vaccine-related lawsuits and initiate a parliamentary investigation into the contaminated vaccines.Lawmakers from the Democratic Party also plan to question the announcement regarding the contaminated vaccine issue during next week's session. As the majority party, they are expected to counter the opposition's criticisms by emphasizing the necessity of vaccinations during the peak of the COVID-19 pandemic.Regarding the drug pricing restructuring, which the Ministry of Health and Welfare (MOHW) plans to implement in July following approval by the Health Insurance Policy Deliberation Committee this month, inquiries are expected to focus on whether the system adequately encourages and fosters innovation within the domestic pharmaceutical and biotech industry.In fact, Rep. Kim Yoon of the Democratic Party previously criticized the MOHW's plan as "too mechanical" and insufficient for rewarding the innovativeness of domestic pharmaceutical companies, and subsequently demanded the submission of a revised proposal.Despite persistent protests from the Korean pharmaceutical industry against the restructuring plan, the MOHW is maintaining its position in its policy to secure Health Insurance Policy Deliberation Committee approval in March.The MOHW plans to hold a one-point subcommittee meeting on the drug pricing restructure next week, followed by a final vote at the plenary session at the end of the month. Detailed calculation rates for generic drugs and preferential pricing measures for innovative pharmaceutical companies are expected to be finalized within this month.The MOHW has proposed reducing the generic pricing rate from the current 53.55% to the 40%, while the pharmaceutical industry views 48% as their bottom line or maximum acceptable cut.Furthermore, the industry argues that the criteria and mechanisms for preferential pricing must be significantly revised to reflect contributions to the development of the domestic industry and to the manufacturing, production, and distribution of high-quality medicines, in order to achieve the Ministry's policy goals.An official from a Health and Welfare Committee member’s office commented, "Since the New Year's business reports have been delayed and the bill subcommittees have not met properly for months, holding the standing committee in March is essential," adding , "The People Power Party has agreed to participate, and I understand that pending issues like the COVID-19 vaccine contamination played a role in that decision."

- Policy

- GSK’s Nucala-Omjjara enters pricing negotiations for reimb in Korea

- by Jung, Heung-Jun Mar 09, 2026 08:53am

- [GSK Korea’s new myelofibrosis drug Omjjara (momelotinib) and the eosinophilic disease treatment Nucala Autoinjector (mepolizumab) have entered drug price negotiations with the National Health Insurance Service (NHIS).In addition, Janssen Korea’s new multiple myeloma treatment, Darzalex SC injection (daratumumab), is also proceeding with price negotiations, the final stage of reimbursement listing.According to industry sources on the 6th, new drugs that passed the Drug Reimbursement Evaluation Committee (DREC) in January have entered the negotiation process with the NHIS.Both Omjjara and Nucala passed the DREC with the condition that reimbursement would be accepted only if the price is set below the committee’s evaluation amount. AI-generated imageOmjjara Tab (100, 150, and 200 mg) was deemed adequate for reimbursement as a treatment for intermediate- or high-risk myelofibrosis in adults with anemia. Nucala Inj was deemed adequate for reimbursement as an add-on maintenance therapy for the treatment of severe eosinophilic asthma in adults and adolescents that is inadequately controlled with existing treatments.With GSK receiving reimbursement approval for two new drugs simultaneously, expectations are rising on the possibility of their concurrent listing.Omjjara passed the Cancer Disease Deliberation Committee review last March but faced delays in reaching the DREC due to issues such as the selection of comparator drugs, requiring a resubmission. It cleared the DREC hurdle approximately 10 months after resubmission.Meanwhile, the Nucala Autoinjector, a new formulation of the drug, is a self-injectable device that allows patients to administer the treatment at home. If reimbursement coverage is expanded to include the self-injection formulation, Nucala’s prescription market presence is expected to grow.At the previous DREC meeting, both Omjjara and Nucala were approved with the condition that reimbursement is appropriate only if the company accepts a price below the evaluated amount. Since the pharmaceutical company has accepted this condition, negotiations with the NHIS are expected to focus on details such as the projected claims amount.Meanwhile, Janssen Korea’s Darzalex SC Inj was recognized as appropriate for reimbursement for ‘combination therapy with bortezomib, cyclophosphamide, and dexamethasone in newly diagnosed light-chain amyloidosis patients.’Unlike Omjjara and Nucala, Darzalex did not receive the “below evaluation price” condition from DREC, allowing it to proceed directly to price negotiations.Following its approval by the CDDC in the latter half of last year, the subcutaneous injection formulation of Darzalex is steadily gaining access to tertiary hospitals in Korea.

- Policy

- Pharmaceutical Act prohibiting non-face-to-face wholesaling

- by Lee, Jeong-Hwan Mar 09, 2026 08:53am

- The amendment to the Pharmaceutical Affairs Act, prohibiting non-face-to-face care platforms from concurrently operating as pharmaceutical wholesalers, is expected to be passed in its original form without revisions.Analysis suggests that related personnel, including Representative Choo Mi-ae, Chairperson of the Legislation and Judiciary Committee, and Representative Han Jeoung-ae, Chair of the Democratic Party's Policy Committee, have maintained a firm commitment to the original bill, which had been stalled at the plenary session for several months after being initially scheduled for processing late last year.The legislation had previously passed the Health and Welfare Committee and the Legislation and Judiciary Committee with agreement between both parties. However, it was repeatedly excluded from the plenary agenda due to opposition from certain lawmakers and the Ministry of Small Businesses and Startups.According to officials from the National Assembly and the pharmaceutical industry, the Pharmaceutical Act prohibiting non-face-to-face care platforms from concurrently operating as pharmaceutical wholesalers is likely to pass the National Assembly plenary session this month.The amendment is aimed at preventing conflicts of interest that arise when a non-face-to-face platform also acting as a wholesaler. If a platform acts as an intermediary for non-face-to-face treatment while also functioning as a wholesaler, a conflict of interest can arise. This is because the platform would be directly involved in prescribing, preparing, and distributing the medications it manages. Additionally, this setup raises concerns that the system could be misused as a method for providing rebates on illegal medications.Some Representatives characterized the bill as the "Doctor Now Prevention Act" and argued it would stifle innovation in the telemedicine sector. Accordingly, this bill was delayed for the National Assembly consideration.In this process, a sharp difference in positions between the relevant government agencies, the Ministry of Health and Welfare (MOHW) and the Ministry of SMEs and Startups, emerged, leading to suggestions that mediation by the Prime Minister's Office and the Office of the President was necessary.However, Ministry of Health and Welfare Minister Jung Eun Kyeong maintained firmly on passing the original version to ensure institutional safety and block market distortions. Within the Democratic Party, voices grew to maintain the original bill, with leadership emphasizing that revised proposals should not compromise the legislative process.In fact, ruling party lawmakers, including Democratic Party Chairman Jung Cheong-rae and Rep. Choo Mi-ae, visited the General Assembly of the Korean Pharmaceutical Association and promised to pass pharmacy-related legislation, including a bill to prevent intermediary platforms from concurrently operating wholesale businesses. Consequently, it is likely that the bill will be considered and processed during this month's plenary session.An official from a Democratic Party lawmaker’s office commented, "From the start, the bill that passed the Legislation and Judiciary Committee was not a matter where amendments should have been discussed, or its tabling in the plenary session was repeatedly excluded without a specific reason." The official added, "While there were some differing opinions within the party, the floor leadership stayed committed to passing the original version."

- Company

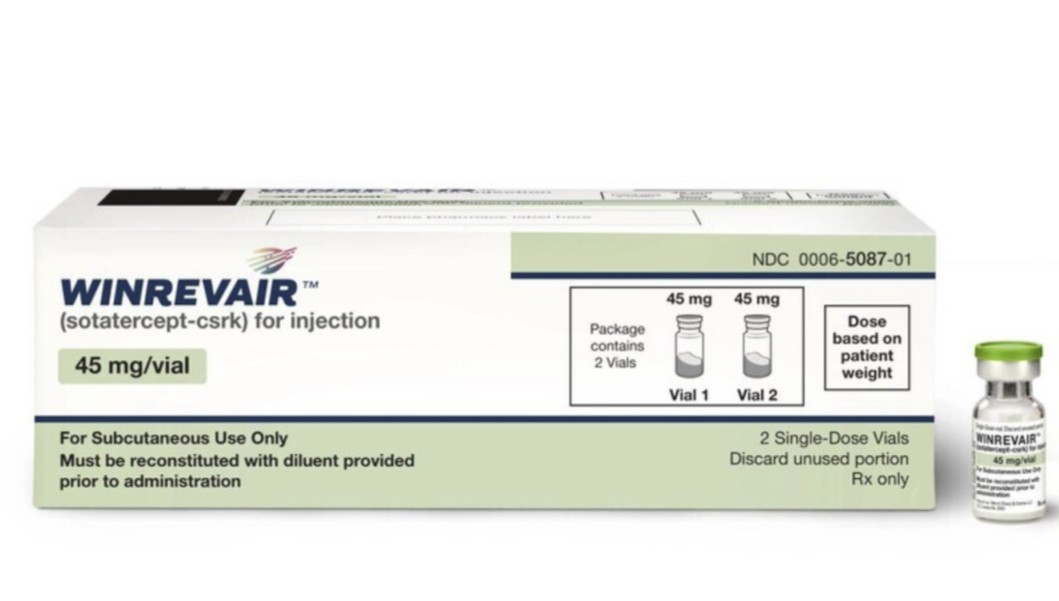

- PAH drug Winrevair may be prescribed at general hospitals in Korea

- by Eo, Yun-Ho Mar 09, 2026 08:53am

- The new pulmonary arterial hypertension (PAH) drug Winrevair is beginning to gain prescribing access at major hospitals in Korea.According to industry sources, MSD Korea’s activin signaling inhibitor (ASI) Winrevair (sotatercept has passed the drug committee (DC) reviews at leading tertiary hospitals, including Samsung Medical Center and Seoul National University Hospital.At the same time, MSD is currently conducting landing procedures at about 20 major medical institutions nationwide.Winrevair is a first-in-class innovative drug with a new mechanism of action, emerging 20 years after sildenafil, which targets the NO–sGC–cGMP pathway, was introduced in 2005. The drug is currently selected for the second phase of Korea’s ‘Approval-Evaluation-Negotiation Concurrent Pilot Program’ and is undergoing reimbursement procedures, but no significant progress has been made so far.Pulmonary arterial hypertension is a particularly challenging area for new drug development. Unlike existing treatments focused on dilating blood vessels, Winrevair improves vascular remodeling, the fundamental cause of the disease.Consequently, no comparable therapeutic alternative is available. If Winrevair is evaluated within the existing economic assessment framework, it would be compared to treatments developed two decades ago. This situation naturally delays the listing process. This challenge is not unique to Winrevair but is one commonly faced by drugs included in the parallel pilot program. Nearly 200 days have already passed since Winrevair received approval from Korea’s Ministry of Food and Drug Safety.Therefore, attention is now focused on whether Winrevair will successfully complete the reimbursement listing process and ultimately establish itself as a treatment option for patients.Winrevair received regulatory approval based on the STELLAR clinical trial. This study evaluated the efficacy and safety of Winrevair in 323 adult patients with pulmonary arterial hypertension (PAH) classified as WHO functional class (WHO-FC) II or III. During the 24-week study period, patients received Winrevair or a placebo in combination with their existing therapy once every three weeks.Results showed that Winrevair increased the 6-minute walk distance by 40.8 meters (Hodges–Lehmann estimate) compared with placebo at Week 24. It also reduced the risk of clinical worsening or death by 84%.In addition, significant improvements were observed across 8 secondary endpoints, including WHO-FC, pulmonary vascular resistance (PVR), and the heart failure biomarker NT-proBNP, compared with placebo.Wook Jin Jeong, President of the Korean Society of Pulmonary Hypertension (Professor of Cardiology at Gachon University Gil Medical Center), said, “Winrevair is a treatment with a new mechanism of action that restores abnormal pulmonary vascular structure toward normal. Based on the latest evidence, updated global clinical guidelines now present it as an option for combination therapy in the early phases of treatment. This approval broadens the treatment options available to pulmonary arterial hypertension patients in Korea.”