- LOGIN

- MemberShip

- 2026-06-14 08:30:06

- Company

- Drug price pressure from US…"K-similars may need to join GENEROUS model"

- by Kim, Jin-Gu Mar 25, 2026 07:21am

- As the U.S. pharmaceutical policies under the Trump administration have been rapidly shifting, suggestions have emerged that South Korean biosimilar companies should consider participating in the CMS (Centers for Medicare & Medicaid Services) new drug pricing model, 'GENEROUS,' as a strategic breakthrough.Professor Dong-chul Seo, Professor Emeritus at Chung-Ang University College of Pharmacy, advised this on the 23rd during a seminar held at the Korea Pharmaceutical and Bio-Pharma Manufacturers Association (KPBMA) titled 'Changes to Pharmaceutical Policy in the Second Trump Administration and Response Strategies for Domestic Companies in South Korea.'Professor Seo analyzed that the GENEROUS model could offer Korean firms an opportunity amid the unpredictable tariff risks of Trump's second presidency and the pressure for Most Favored Nation (MFN)-based price reductions.The GENEROUS (Generating Cost Reductions for U.S. Medicaid) model is a pilot program designed by CMS to reduce costs for U.S. Medicaid. Scheduled to run for five years starting in 2026, this model's key is the application of MFN pricing based on companies' 'voluntary participation'.Participating companies must provide additional rebates to Medicaid referencing the second-lowest price among eight reference countries (UK, France, Germany, Italy, Canada, Japan, Denmark, and Switzerland). Unlike the Inflation Reduction Act (IRA), which mandates price reductions, this is closer to a negotiation-based model in which companies accept price cuts in exchange for securing status in the nation's public insurance programs.CMS introduced this model to lower patients' out-of-pocket costs by reducing drug prices. CMS calculates the Guaranteed Net Unit Price (GNUP) based on the MFN price. Pharmaceutical companies must meet this standard by adding extra rebates to existing ones. State governments accept the prices negotiated by CMS with manufacturers, and further price-reduction negotiations are restricted.Professor Seo stated, "This system is designed to provide additional rebates to the government if foreign drug prices are lower," adding, "Since it is a voluntary participation method with applications accepted until the 30th of next month, companies can review their participation."Analysis suggests that the GENEROUS model may favor biosimilars, as it secures standing in public insurance on the premise of price reductions.For original drugs, accepting MFN pricing is difficult due to the burden of maintaining global pricing tiers. Conversely, biosimilars, which have already been competing at lower price points, are differentiated by the possibility for additional reductions. Accordingly, this is seen as an opportunity to expand market share in the Medicaid market, where the influence of original drugs is diminishing.There is also the possibility of using this as a tool to counter tariff risks. The Trump administration previously proposed 'tariff exemptions for the next three years' to 16 global pharmaceutical companies that agreed to supply at MFN prices. Other mentioned benefits include the provision of FDA's National Priority Vouchers and the application of 'PreCheck' programs. As the GENEROUS model is also a program predicated on fiscal savings, similar policy incentives may be granted.However, suggestions have been made that precise profit-and-loss calculations are needed, given the inherent unpredictability of the Trump administration's pharmaceutical policies. This means a thorough review is required to see if the volume increase from market share expansion outweighs the price cuts and potential tariff burdens.Professor Seo stated, "It would be beneficial for Korean biosimilar manufacturers to participate in this model and experience the actual price application methods," and suggested, “Since generics and biosimilars are highly price-sensitive and have relatively limited global price-linkage effects, participation in the GENEROUS model can be reviewed."Professor Seo further stated, "Companies must comprehensively consider their Medicaid market dependency and sales proportions, the risk of exposing reference country price in MFN is applied, and the impact of price linkages in other nations," and concluded, "Participation may require systematic management of global price exposure and its subsequent effects.”

- Policy

- Pharma companies may suffer KRW 600B annual loss shock

- by Lee, Jeong-Hwan Mar 25, 2026 07:21am

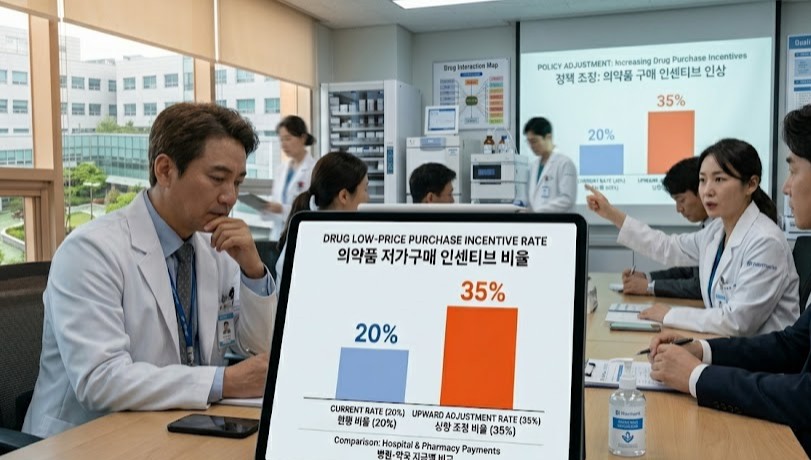

- The Ministry of Health and Welfare (MOHW)'s 'drug pricing system reform plan' to raise the low-price purchasing incentive rate for hospitals and pharmacies from 20% to 35%. Concerns about pharmaceutical industry shock.The government's 'drug pricing system reform plan' to raise the low-price purchasing incentive rate for hospitals and pharmacies from 20% to 35% is facing criticism. Critics pointed out that it is an administrative move that will increase pharmaceutical companies' losses.The pharmaceutical industry is already enduring approximately KRW 350 billion in annual revenue losses under the 20% incentive system. Concerns are rising that if the government transitions to a market-linked actual transaction price system by expanding the incentive rate to 35%, annual losses will exceed KRW 600 billion, inevitably causing market contraction.Given that the government already implements price cuts for existing generic drugs, analysis suggests that raising the low-price purchasing incentive rate will further worsen pharmaceutical companies' profitability, potentially threatening the production and stable supply of essential medicines.On the 24th, the Ministry of Health and Welfare (MOHW) announced a regulation raising the incentive rate paid to medical institutions and pharmacies for low-priced purchasing from 20% to 35% as part of the actual transaction price-based price reduction method. This reform aims to restructure the current system into a market-linked actual transaction price model.The low-price purchasing incentive is a system in which, if a medical institution or pharmacy purchases a drug from a pharmaceutical company at a price below the government-set insurance ceiling price, a portion of those savings is returned to the institution as an incentive.Under the current 20% rate, if a hospital purchases a drug at KRW 100 below the reference price (ceiling price), it receives a KRW 20 incentive.While systemically designed to improve purchasing efficiency and save the National Health Insurance budget, the system has been criticized for pressuring pharmaceutical companies to reduce prices.The pharmaceutical industry estimates that current losses amount to KRW 350 billion annually under the 20% rate. Based on this, pharmaceutical industry argues that a 35% incentive rate would result in annual drug revenue losses to KRW 600 billion or more.Furthermore, assessments suggest that if the price-reduction mechanism for actual transaction price investigations fails to operate properly despite the 35% rate, pharmaceutical companies could face actual losses exceeding these calculations.Concerns are rising that the overall profit base of the pharmaceutical industry could be destabilized if additional price pressures, such as the increased incentive rate, are added to the Ministry's general policy of cutting prices for listed drugs.The MOHW's proposal to raise the incentive rate (from 20% to 35%) is seen as a measure that strengthens the mechanism for transferring price-cutting pressure to manufacturers. Hospitals and pharmacies will have a greater incentive to purchase drugs at the lowest possible prices to secure larger rewards, which may put pressure on pharmaceutical companies to lower their supply prices.An official from a mid-sized Korean pharmaceutical company stated, "While the official insurance drug price may remain the same, the structure forces actual transaction prices to keep falling. If the incentive rate is raised, hospitals, which have more authority, will demand stronger price cuts. Pharmaceutical companies may face significant burdens."The official added, "The current actual transaction price reduction system and the 20% incentive rate must be maintained so that it can alleviate the excessive burden on the industry," and emphasized, "Raising the incentive rate exacerbates the issue of increased losses, especially when a pharmaceutical company sells more. This may ultimately force certain companies to abandon the stable supply of essential medicines."

- Policy

- Stelara biosimilar ‘Epyztek Pen’ listed for reimb next month

- by Jung, Heung-Jun Mar 25, 2026 07:21am

- The pen formulation of Samsung Bioepis’s autoimmune disease treatment Epyztek (ustekinumab) is scheduled to become the first reimbursed product of its ingredient class next month.Samsung Bioepis appears to be pursuing a differentiation strategy with a pen formulation that even the original product, Janssen Korea’s ‘Stelara,’ has neither received approval nor reimbursement for.According to industry sources on the 24th, Samsung Bioepis will expand its reimbursement lineup next month with a prefilled pen formulation of its Stelara biosimilar Epyztek.Like Stelara, Epyztek is an autoimmune treatment indicated for plaque psoriasis, psoriatic arthritis, Crohn’s disease, and ulcerative colitis. In South Korea, it competes in the market alongside Celltrion’s biosimilar ‘Steqeyma’ and others.The pen formulation, scheduled for listing next month, allows patients to administer the medication conveniently and accurately, giving it a competitive edge in self-administration settings.Stelara is currently approved only in intravenous, subcutaneous, and prefilled syringe formulations, making the prefilled pen the first of its kind among products with the same active ingredient. Samsung Bioepis secured its place on the reimbursement list just 3 months after receiving approval from the MFDS last January.This preemptive addition of a new formulation is expected to continue its offensive not only against biosimilar competitors but also in the battle for market share against the original product.Samsung Bioepis is targeting the market with a price lower than the original. The newly listed Epyztek Prefilled Pen 90 mg/1 mL is expected to receive an insurance ceiling price in the KRW 1.27 million range.The original Stelara Prefilled Syringe 45 mg/0.5 mL is priced at KRW 1,745,600, while Epyztek Prefilled Syringe at the same dose is about 30% cheaper at KRW 1,233,376. The pen formulation offers double the dosage but is priced about 27% lower.Leveraging its lower price and the addition of new formulations, the company is expected to begin a full-scale push to expand its market share starting in the second quarter of this year.Samsung Bioepis sells Epyztek (known as Pyzchiva in the U.S. and Europe) not only in Korea but also in Europe and the U.S. through its partner, Sandoz.

- Company

- Imfinzi approved as perioperative gastric cancer therapy in KOR

- by Son, Hyung Min Mar 25, 2026 07:21am

- Immuno-oncology drug ‘Imfinzi’AstraZeneca Korea (CEO Eldana Sauran) announced on the 23rd that Imfinzi (durvalumab) has received approval for perioperative treatment of gastric cancer in Korea.The approved indication is for the treatment of patients with resectable gastric or gastroesophageal junction adenocarcinoma, as perioperative therapy in combination with 5-fluorouracil, leucovorin, oxaliplatin, and docetaxel (FLOT) chemotherapy before and after surgery, followed by Imfinzi monotherapy as adjuvant treatment.Under the approved regimen, Imfinzi is administered in combination with FLOT (5-fluorouracil, leucovorin, oxaliplatin, and docetaxel) for two cycles before surgery, followed by surgery. After surgery, two cycles of Imfinzi plus chemotherapy are administered, and then maintenance treatment with Imfinzi monotherapy is initiated. With this approval, Imfinzi becomes the first immuno-oncology drug approved in Korea for perioperative treatment of gastric cancer.While surgery is the primary treatment for gastric cancer, recurrence rates have historically been high even after surgical intervention. In fact, about 40% to 60% of gastric cancer patients die from recurrence. It is also reported that among patients who experience recurrence after surgery, 50% recur within two years and 90% within five years.This approval of Imfinzi is viewed as a new therapeutic approach that can reduce the risk of recurrence and provide survival benefits as a perioperative therapy for gastric cancer.The approval was based on results from the global Phase III MATTERHORN study in patients with resectable gastric cancer and gastroesophageal junction adenocarcinoma. The MATTERHORN study evaluated the efficacy and safety profile of Imfinzi plus FLOT chemotherapy followed by Imfinzi monotherapy as perioperative treatment, compared with a control arm that received FLOT chemotherapy and surgery alone.Study results confirmed that Imfinzi demonstrated clinical benefits in terms of the primary endpoint, event-free survival (EFS), as well as the secondary endpoints of overall survival (OS) and pathological complete response (pCR) rates.Perioperative Imfinzi reduced the risk of disease progression, recurrence, or death from any cause by 29%, showing a significant improvement in EFS. At 24 months, overall survival was numerically higher in the Imfinzi perioperative treatment group at 75.7%, compared with 70.4% in the control group, although statistical significance was not established. The pCR rate was also approximately 2.7 times higher, at 19.2% in the Imfinzi group versus 7.2% in the control group.The safety profile of perioperative Imfinzi observed in the MATTERHORN study was consistent with the known safety profiles for each individual agent.Professor Keun-wook Lee of the Department of Hematology and Oncology at Seoul National University Bundang Hospital stated, “Gastric cancer is a type of cancer in which recurrence occurs in a substantial number of patients even when treated at a resectable stage. In particular, it has been reported that a significant number of patients with stage II–III gastric cancer experience recurrence despite receiving adjuvant therapy after surgery, rendering a new treatment strategy encompassing both pre- and post-operative settings urgently needed.”He added, “In the MATTERHORN study, clinical benefit in terms of event-free survival and overall survival versus placebo was confirmed, and the pathologic complete response rate was also 2.7 times higher than with standard treatment, making this a clinically significant finding.”Hyun-joo Lee, Executive Director of the Oncology Business Unit at AstraZeneca Korea, said, “Through the MATTERHORN study, we confirmed, for the first time as an immuno-oncology agent, clinical benefit in perioperative treatment for patients with resectable gastric cancer. Since Imfinzi has been approved for the treatment of gastric and gastroesophageal junction adenocarcinoma based on this study, we are deeply honored to be able to provide a meaningful new treatment option to Korean gastric cancer patients, for whom there has been a significant unmet need.”

- Opinion

- From pharmacy practice to new drug review

- by Jung, Heung-Jun Mar 25, 2026 07:20am

- Even after a new drug is developed and released to the market, there is one hurdle that must be cleared for patients to fully benefit from it: the National Health Insurance reimbursement listing.How this initial step is handled, in reviewing whether a drug should be covered by health insurance, determines both patients’ access to treatment and the balance of Korea’s insurance budget.The organization guarding that crucial gate is the Department of Drug Management of the Health Insurance Review and Assessment Service (HIRA). It is also one of the operational departments where pharmacists can create synergy based on their understanding of pharmaceuticals.Assistant Directors Jae-young Choi (left) and Jin-woo Song of the New Drug Listing Division, Department of Drug ManagementDailyPharm met with Jin-woo Song (38) and Jae-young Choi (34), assistant directors working in the Department of Drug Management, by drawing on their clinical experience in hospitals and pharmacies. We were able to hear their candid thoughts on what their new roles entail after hanging up their pharmacist’s coats, as well as the challenges and satisfactions they face.Both have been with the agency for 1-2 years. What has your career as pharmacists been like?Jin-woo Song (hereinafter Song): After graduating from pharmacy school in 2023, I worked at the Pharmacy Department of Severance Hospital for 2 years. I gained experience in the Inpatient Dispensing Unit, Special Dispensing Unit, Pharmacy Information Unit, and Outpatient Dispensing Unit before joining HIRA last June.Jae-young Choi (hereinafter Choi): I also have experience working as a night-shift pharmacist at a hospital and in a community pharmacy after graduation. I joined HIRA in December 2024, so it’s been just over a year now.Among various career options, why did you choose to join HIRA?Song: While working at the hospital, I realized that I am well-suited to a well-established system-based institution. I became curious about how reimbursement criteria and procedures for pharmaceuticals are set and decided to move to HIRA.Assistant Director Jin-woo SongChoi: After graduation, I became increasingly interested in social pharmacy. I applied because I became interested in new drug listing and management of already listed drugs to improve patient access to treatments. I found the idea of approaching pharmaceuticals from the public sector appealing.Did you prepare anything specifically in order to join HIRA?Song: Since they make the hiring process very convenient for pharmacists, there was nothing specific I needed to prepare. If you have at least 1 year of experience at a university, research institute, pharmaceutical company, hospital, or pharmacy, you only need to submit a cover letter. The written test is waived. As long as you meet the requirements, you can take the interview, and even upon joining, you are hired at Grade 4 (assistant director).What kind of work are you doing in the Department of Drug Management?Song: I have been working in the New Drug Listing Division since June last year. My work involves the overall process related to reimbursement listing for new drugs. I handle cost-effectiveness reviews related to expanded criteria for risk-sharing agreement drugs as well as assessments of the appropriateness of renewing RSAs for such drugs.Choi: I’m part of the Agenda Team within the New Drug Listing Division. I joined in December 2024, so it’s been just over a year. When I’m assigned cases involving new drugs or RSA drugs, such as applications for reimbursement decisions, requests to expand reimbursement criteria, or evaluations related to contract expiration, I review them based on criteria like clinical utility and cost-effectiveness. I then present those results to the Drug Reimbursement Evaluation Committee.How has your experience in hospitals and pharmacies been helpful?Song: I handled many anticancer drugs and medications for severe diseases at a tertiary hospital. Many of the drugs I encountered back then are now being submitted for reimbursement listing. The drug information, reimbursement criteria, and guidelines I referred to while handling information management tasks have been very helpful.Choi: I worked at a pharmacy until just before joining the agency, so there wasn’t much direct overlap with my current duties. However, having studied pharmacy for many years, my background knowledge helps when exploring new areas.Assistant Director Jae-young ChoiHas your perception of HIRA changed since joining?Song: At first, I worried that the rigid organizational culture might be difficult to adapt to. But after experiencing it firsthand, I found that there is a very horizontal and mutually respectful organizational culture.Choi: It wasn’t until I was about to graduate from pharmacy school that I learned there were pharmacists working at HIRA and that they handled drug management tasks. After joining, I realized that the drug-related work HIRA handles is more diverse than I had imagined.What is the most challenging aspect of your work?Song: Newly launched drugs are expensive, so using them as treatments without reimbursement places a heavy financial burden on patients. We receive many requests for reimbursement, but the challenge is that we cannot simply grant the requests of those who are just waiting for reimbursement.Choi: The fact that I have to continuously study new diseases is both the best part and the most challenging aspect of the job.When do you feel a sense of accomplishment?Song: As part of the New Drug Listing Division’s duties, we review the appropriateness of reimbursement at the DREC. I feel a sense of accomplishment when the reimbursement appropriateness of an item I reviewed is approved.Choi: It’s the moment a new drug I’ve reviewed gets actually listed. I still lack experience and have a lot to learn. Going forward, I want to think more deeply about the social impact as I do my work.Do you have any advice for pharmacy students or pharmacists interested in joining HIRA?Song: While you may be fulfilling various roles in hospitals or pharmacies, there are tasks that can only be performed at HIRA. You’ll likely find a sense of fulfillment and accomplishment here that’s distinct from what you’d experience elsewhere.Choi: Given the nature of our work, I feel we’re doing things that are hard to experience elsewhere. If you’re interested in the public sector beyond clinical practice, I encourage you to apply during our recruitment period.

- Policy

- Anticancer drugs account for record high share of pharma expenditures

- by Jung, Heung-Jun Mar 24, 2026 08:16am

- Claims for anticancer drugs are rising steeply within Korea’s national health insurance pharmaceutical expenditures. It exceeded KRW 3 trillion the year before last, surpassing anti-atherosclerosis drugs for the first time.While total drug expenditures rose by 5.6%, claims for anticancer drugs climbed by 15%, the largest increase by far among the 5 five therapeutic classes in terms of spending.Anticancer drug claims exceed KRW 3 trillionAccording to the 2024 Status of Expenditures on Reimbursed Drugs Report released by the National Health Insurance Service on the 23rd, health insurance drug expenditures totaled KRW 27.6625 trillion, a 5.6% increase from the previous year’s KRW 26.1966 trillion.Drug costs accounted for 23.8% of total healthcare expenditure of KRW 116.2375 trillion. As of 2023, the proportion of drug expenditures in Korea’s current health expenditure was 19.4%, which is 5 percentage points higher than the OECD average of 14.4%.Among major overseas countries (A8) that Korea uses for drug price references, Korea’s spending ratio was also higher than Japan (17.6%), Germany (13.7%), and the UK (9.7%).◆ Anticancer drug claims reach KRW 3.1432 trillion... share hits record high of 11.4%Claims and spending share for anticancer agents reached all-time highs. Claims totaled KRW 3.1432 trillion in the year before last, up 15% from KRW 2.7336 trillion the previous year.The top 5 therapeutic classes accounted for 40.4% of total drug expenditure, with anticancer drugs holding the largest share at 11.4%. Until now, anti-atherosclerotic drugs had previously held the highest claim amount and market share, but anticancer drugs rose to the top spot for the first time.Drug costs for cancer patients totaled KRW 4.2958 trillion, an 11.9% increase from the previous year. This marks the largest growth rate in the past 5 years.◆ By ingredient, “ezetimibe + rosuvastatin” ranked highest…up 16% to exceed KRW 700 billionBy ingredient, spending on ezetimibe + rosuvastatin rose 16.3% year on year, reaching KRW 704.6 billion.Choline alfoscerate came in second at KRW 557.6 billion, down 1% from the previous year. Atorvastatin also declined slightly, with claims of KRW 554.3 billion, down 0.8%. The antiplatelet agent clopidogrel reached KRW 441.8 billion, up 5.7%.◆ Decline in original drug claims...generic share rises to 44.4%Original drug claims showed a declining trend, while generic claims increased. In the year before last, spending on original drugs amounted to KRW 15.3434 trillion, accounting for 55.6% of total pharmaceutical expenditure, down from 59.1% the year before.In contrast, generic drug claims totaled KRW 12.2591 trillion. This accounted for 44.4% of total drug expenditure, an increase from 40.9% the previous year.Since 2021, the spending share of original drugs has continued to decline while that of generics has risen, narrowing the gap in reimbursement claims between the two categories.An NHIS official said, “In line with government policy direction, we will further refine implementation measures and actively support the execution of tasks for the benefit of the public and the development of the pharmaceutical industry, while making every effort to ease patients’ drug cost burdens and ensure the financial sustainability of the National Health Insurance system.”

- Policy

- Will Mifegyne gain momentum for Korean entry?

- by Lee, Jeong-Hwan Mar 24, 2026 08:16am

- The domestic introduction of Mifegyne, the abortion drug whose marketing approval by the Ministry of Food and Drug Safety has been delayed for a long time, is expected to gain momentum.This follows recent remarks by Yong-jin Park, vice chair of the Regulatory Reform Committee, who identified the delay in Mifegyne’s approval as a prime example of irrational administrative regulation and announced his intention to work toward a solution.Vice Chair Park is reportedly determined to ensure domestic approval through administrative action even before legislation is enacted, given that the introduction of Mifegyne is regarded as a matter of national policy.Vice Chair Yong-jin ParkVice Chair Park views the issue of Mifegyne’s introduction from a global standards perspective. He argues that the situation where only Korea is blocking a drug already permitted in over 100 countries worldwide, including OECD nations, solely due to administrative procedures, represents an irrational regulation unique to Korea.Vice Chair Park believes that the reality where women are forced to purchase the drug through underground channels despite its globally proven safety due to administrative barriers threatens women’s health rights and must not be ignored.The MFDS has maintained a cautious stance on approving Mifegyne on the grounds that follow-up legislation has not yet been made since the Constitutional Court’s 2019 decision declaring the abortion law unconstitutional.Vice Chair Park believes that if the MFDS takes a more forward-looking approach to the regulatory barriers it has tied itself to, a solution can be found.This effectively suggests the need to expedite the timing of domestic approval and introduction through proactive government action, even before the legislature completes the relevant process.Attention is now focused on whether the drug could be approved before the National Assembly passes a proposed revision to the Mother and Child Health Act, introduced by Democratic Party of Korea lawmaker In-soon Nam and others, that would allow medication-induced abortion.If the MFDS adopts administrative regulations or establishes a separate approval process, the official introduction of Mifegyne in Korea will gain momentum.An industry official stated, “If Vice Chairman Park’s plan to ease administrative regulations is effectively implemented, the MFDS will be able to exercise proactive administration even amid a legislative vacuum. It would become a representative example of the government putting forward a preemptive alternative at the administrative level.”

- Policy

- Afilivu’s price cut and lists PFS formulation to chase Eylea

- by Jung, Heung-Jun Mar 24, 2026 08:16am

- Samsung Bioepis is stepping up its pursuit of Eylea by lowering the price of its macular degeneration treatment Afilivu and expanding into the prefilled syringe (PFS) segment.Next month, Afilivu Prefilled Syringe 6.6 mg/0.165 mL (aflibercept) will be listed for reimbursement, and the price of the existing Afilivu injection will be voluntarily cut to KRW 198,000, matching the market’s lowest price.According to industry sources on the 23rd, Samsung Bioepis is simultaneously pursuing both a price reduction and the addition of a new formulation to strengthen Afilivu’s competitiveness.Samsung Biologics expands Aflilivu's competitivity by introducing a PFS version with reimbursement. AI-generated imageThe ceiling price of Afilivu 40 mg, previously KRW 298,000, will be voluntarily reduced by KRW 100,000 to KRW 198,000.This matches the lowest price set by Sam Chun Dang Pharm’s Eylea biosimilar ‘Vgenfli Inj.’The Afilivu PFS formulation entering reimbursement this time has also been listed at the same price of KRW 198,000. Not only Eylea, but also Celltrion’s Eydenzelt and Sam Chun Dang Pharm’s Vgenfli already have PFS formulations in their reimbursement lineups.Celltrion also expanded its prescription lineup by listing the PFS formulation last November. Although the Afilivu PFS formulation is a later entrant compared to these, it appears the company will launch a full-scale market offensive by lowering its price.Sales of Afilivu in Korea were suspended early last year due to a preliminary injunction filed by the original developer, Regeneron, seeking to halt sales. However, after the injunction was overturned in December of the same year, domestic distribution and sales resumed. Samil Pharmaceutical holds the exclusive domestic sales rights.It is said to have shown a rapid recovery in sales since resuming distribution. Samil is expected to continue expanding prescriptions through sales activities that now include the PFS formulation.The domestic Eylea market is estimated at about KRW 100 billion. Samsung Bioepis, Celltrion, and Sam Chun Dang Pharm are all closely chasing Eylea and competing to expand market share.In particular, fierce competition is expected between Samsung Bioepis and Sam Chun Dang Pharm, as they are clashing with a lowest-price strategy.

- Policy

- Menarini withdraws approval for angina drug Ranexa

- by Lee, Tak-Sun Mar 24, 2026 08:16am

- ‘Ranexa (ranolazine), a new angina treatment with a novel mechanism of action that had garnered high expectations as the first of its kind in over 20 years, has given up on entering the Korean market five years after its local approval.Used as a second-line treatment for angina, the drug had remained approved but never been listed for reimbursement. As a result, it appears that the company decided to withdraw the product once the re-examination period expired.According to the Ministry of Food and Drug Safety, Menarini Korea voluntarily withdrew marketing authorization for three strengths of Ranexa extended-release tablets—375 mg, 500 mg, and 750 mg, as of the 23rd. Having obtained domestic approval in March 2020, the drug never made it to market and has now disappeared from the regulatory records after five years.Unlike existing beta-blockers or calcium channel blockers (CCBs), Ranexa garnered attention for its unique mechanism of action, which selectively inhibits sodium channels within cardiac muscle cells. Because it does not significantly affect blood pressure or heart rate, it has been considered an alternative for patients whose symptoms are difficult to control with existing medications.However, it never made it onto the national health insurance reimbursement list after approval. To make matters worse, the re-examination period granted at the time of approval reportedly expired on the 15th.Although three months remained before the application period for re-examination closed, the company appears to have chosen to withdraw the approval rather than pursue re-examination. Since no actual sales took place after approval, it is assumed that conducting a re-examination would also have been difficult.The drug was approved by the US FDA in January 2006. At the time, it was the first new angina treatment to gain approval in the United States in more than 20 years, drawing considerable attention.While it was approved in the US. as a first-line treatment for chronic angina, it was approved as a second-line treatment when it received approval in Europe. On July 9, 2008, the European Medicines Agency (EMA) approved it as an add-on therapy for first-line stable angina treatment.When it received domestic approval on March 16, 2020, the indications were also determined based on the European approval. Menarini Korea conducted bridging studies and other procedures to obtain domestic approval for this drug, ultimately receiving approval one year and eight months after filing.Low market potential is cited as the reason for withdrawing from the domestic market. With existing angina treatments already priced low, it is believed that Ranexa, as a second-line therapy, also faced an environment in which it would be difficult to secure a sufficiently high reimbursement price.Currently, there are no generics containing the same active ingredient available. Consequently, medications containing ranolazine are no longer available in Korea.An industry official said, “When a new drug gives up entering the Korean market because of marketability issues, it ultimately only lowers treatment accessibility for patients. When a new drug is withdrawn, it is necessary to closely examine whether there are any generics with the same ingredient or alternative medicines available.”

- Company

- Evrysdi reimb expansion will improve SMA treatment landscape

- by Son, Hyung Min Mar 24, 2026 08:16am

- The expansion of reimbursement criteria for the spinal muscular atrophy (SMA) treatment Evrysdi is expected to significantly improve treatment convenience for SMA patients in Korea.Experts note that the introduction of the tablet formulation, the extension of the prescription period, and the allowance for switching between therapies have reduced the burden of long-term therapy and increased the sustainability of treatment in daily life.On the 23rd, Roche Korea held a press conference at its headquarters in Gangnam-gu, Seoul, to commemorate the launch of the tablet formulation of its SMA treatment Evrysdi (risdiplam) and the expansion of the drug’s reimbursement criteria.Evrysdi is the only oral treatment among SMA therapies and is regarded as a drug that has brought about a shift in the treatment landscape, which was previously dominated by injectable formulations. This contrasts with Biogen’s Spinraza (nusinersen) and Novartis’s Zolgensma (onasemnogene abeparvovec), both of which are injectable therapies.Since its first approval in Korea in 2020 as a dry syrup formulation and subsequent reimbursement in 2023, a tablet formulation was later approved. Starting this March, the tablet formulation became eligible for reimbursement, and the existing reimbursement criteria were expanded.The key elements of the revised reimbursement criteria include: ▲ allowing one-time bidirectional substitution with injectable therapies ▲ extending the maximum prescription period to approximately 2 months ▲ and refining assessment tools to better reflect the patient’s condition.Previously, prescriptions for the dry syrup were limited to 3 bottles (a 36-day supply), effectively allowing only monthly prescriptions; however, following the revision, the reimbursement criteria have been expanded to a maximum of 5 bottles (a 64-day supply). Prescriptions for tablet formulations can now also be issued for up to 2 packs (56 days’ supply), helping to reduce the treatment burden on patients and their caregivers.Jong-Hee Chae, Professor of Pediatrics at Seoul National University HospitalIn addition, whereas previously only a one-time switch from Spinraza to Evrysdi was allowed, the revision now permits bidirectional switching, greatly expanding flexibility in treatment strategy.Jong-Hee Chae, Professor of Pediatrics at Seoul National University Hospital (Chair, Korean Child Neurology Society), said, “In the past, once a treatment was selected, it was difficult to change, but now we can apply more flexible strategies based on the patient’s age, environment, and treatment response.”She added, “With the assessment tools now more finely subdivided, it has also become possible to evaluate treatment effects more precisely in a way that reflects each patient’s actual condition.”SMA is a rare genetic disorder characterized by the gradual loss of motor neurons due to a deficiency of the survival motor neuron (SMN) protein, affecting respiration, swallowing, and overall motor function. It is classified into Types 1 through 4 based on the age of onset and functional level, with Type 1 being a particularly severe form with high mortality if untreated.Professor Chae said, “Because SMA is a disease that requires long-term treatment, it is crucial to ensure the sustainability of treatment in daily life. The introduction of tablets that can be stored at room temperature and the extension of the prescription period represent meaningful changes in improving the quality of life for patients and their families.”Long-term effects confirmed through real-world dataEvrysdi has also shown sustained effectiveness in real-world data (RWD).This drug is a small molecule that modulates SMN2 gene splicing, and it works by crossing the blood-brain barrier and increasing production of the SMN protein throughout the body, including the central nervous system.Hyungjun Park, Professor of Neurology at Gangnam Severance HospitalConsistent efficacy has been confirmed across 4 global clinical trials, ranging from infants before symptom onset to patients with prior treatment experience. Notably, in Types 1 and 2/3 patients, long-term data spanning over 5 years demonstrated the maintenance of motor function.Similar results were also confirmed in real-world data (RWD) recently published in Europe. In a study of patients in the Czech Republic and Slovakia, early improvements in motor function were observed even in severely affected patients, along with the maintenance of respiratory and motor function for up to 3 years.In another Croatian study, patients who switched from an existing injectable therapy to Evrysdi showed motor function improvement over 12 months comparable to prior treatment, confirming non-inferiority.Hyungjun Park, Professor of Neurology at Gangnam Severance Hospital, said, “Recent real-world data from Europe show that Evrysdi exhibits a pattern of significant functional improvement within the first 6 months of treatment, followed by stable maintenance over the long term. In particular, improvements and maintenance of motor function were confirmed in patients with SMA Types 2 and 3, and results showing stable maintenance without functional decline were also confirmed in Type 1 patients.”He further emphasized, “Given the natural course of SMA, which is characterized by continued functional deterioration, this represents a meaningful change. Because consistent efficacy and long-term durability have been confirmed across a wide range of patient groups, the drug has strong practical value in real-world clinical practice.”